It’s a story that gets trotted out every few years by mutual fund managers and the brokers who sell them.

“It’s a stock-pickers market!”

They’ll then go on to talk about “falling stock correlations” and how they will now be able to beat the market. The reason they couldn’t beat the market last year is that stocks were moving in “lockstep” and it didn’t matter what they picked. (This is the closest thing a fund manager will ever come to admitting they cannot do what they charge investors to do.)

Two big problems with this. The chart below shows rolling stock correlations since 1990. High stock correlations imply a “difficult” market for stock pickers, low stock correlations imply an “easy” market.

In late 2011, correlations surged as markets got skittish. So, do opportunities to pick stocks disappear as correlations go up?

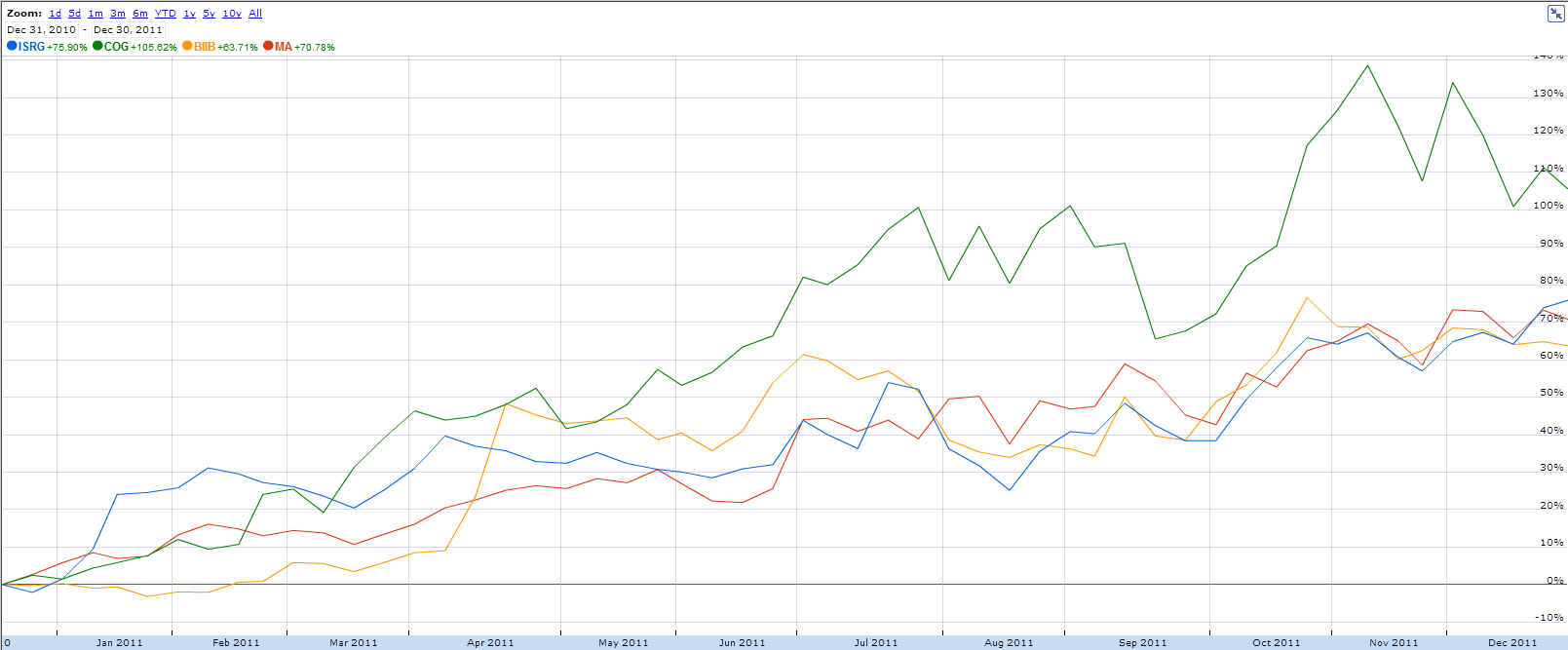

Here’s the best-performing stocks for calendar year 2011, up 60-100% on the year.

And here’s the worst five stocks of 2011, down -60% to -80%.

So there’s a 100%+ spread between the best stocks and worst stocks in a year with higher-than average correlations. Some opportunity there to beat the market, I would assume. How’d they do? In 2011, 81.28% of large-cap US mutual funds underperformed their benchmark (via SPIVA). I guess they were right, high correlations led to a bad environment for fund managers (despite huge spreads between the best and worst stocks in any year).

Taking a longer-term view, how do the numbers stack up? If stock correlations are low, do fund managers have a better shot? I looked at data over the last several years. From the correlation chart above, we’ll look at the beginning year stock correlation and subsequently how many large cap US managers were beaten by the S&P 500.

Visually the data is inconclusive. Active managers took a beating from 2010-2012 and stock correlations rose. But stock correlations also rose in ’08-’09 with no real impact. In other years (’02-’03) correlations were relatively low and manager performance was dismal.

So, let’s be done with this meme. Even higher correlations leave plenty of dispersion in stock returns, and when correlations drop, manager performance doesn’t necessarily improve. No such thing as “a stock picker’s market.”