In The Markets

After months and months of market gains, risk is suddenly back on everyone’s mind. During the third quarter, large cap US stocks managed to squeak by with a small gain, but many other asset classes saw losses.

US Small cap stocks (-7.36%) and developed (-5.88%) and emerging foreign markets (-4.33%) were negative for the quarter. US Real Estate (measured by the Morningstar Real Estate category) was down -2.87% as well. For most asset classes, these declines occurred in the month of September. Generally speaking, bonds fared better with the Barclay’s Aggregate Bond up 0.17% and the Barclays Municipal bond benchmark up 1.49% for the quarter. Across the spectrum, long term bonds outperformed short term bonds as interest rates mostly held steady.

Despite a disappointing quarter, some broad markets are still positive for 2014, including large cap US Stocks (8.34% YTD), Real Estate (14.16% YTD) and bonds (4.10% YTD).

As I mentioned last quarter and also commented elsewhere earlier this year, we have experienced an unusually calm period in the markets for quite some time. Whether or not we are “due” for a correction is irrelevant – more relevant is how we as investors will behave when a correction inevitably comes. September was an excellent reminder that investing in global stocks comes with its share of volatility and markets do not go up in a straight line forever. Temporary drops in stock prices are a natural part of long-term investing. As easily as market prices can run up, they can also come down. We are here for the long term – to participate in the eventual growth of global capitalism and capture as much of that return as we can. We should not at all be concerned by modest drops in portfolio values over brief periods of time (and I should acknowledge that a “brief” period of time for long-term investors can easy be more than a year). Temporary changes in the prices of stocks in your portfolio should have no impact on your investment strategy as a long term investor.

Economic News

Any economic updates seem to be on repeat for the last several quarters. We continue to see slow and modest improvements across most segments of the economy. In August, consumer spending grew 0.5% and wages grew 0.4%, supporting this thesis.

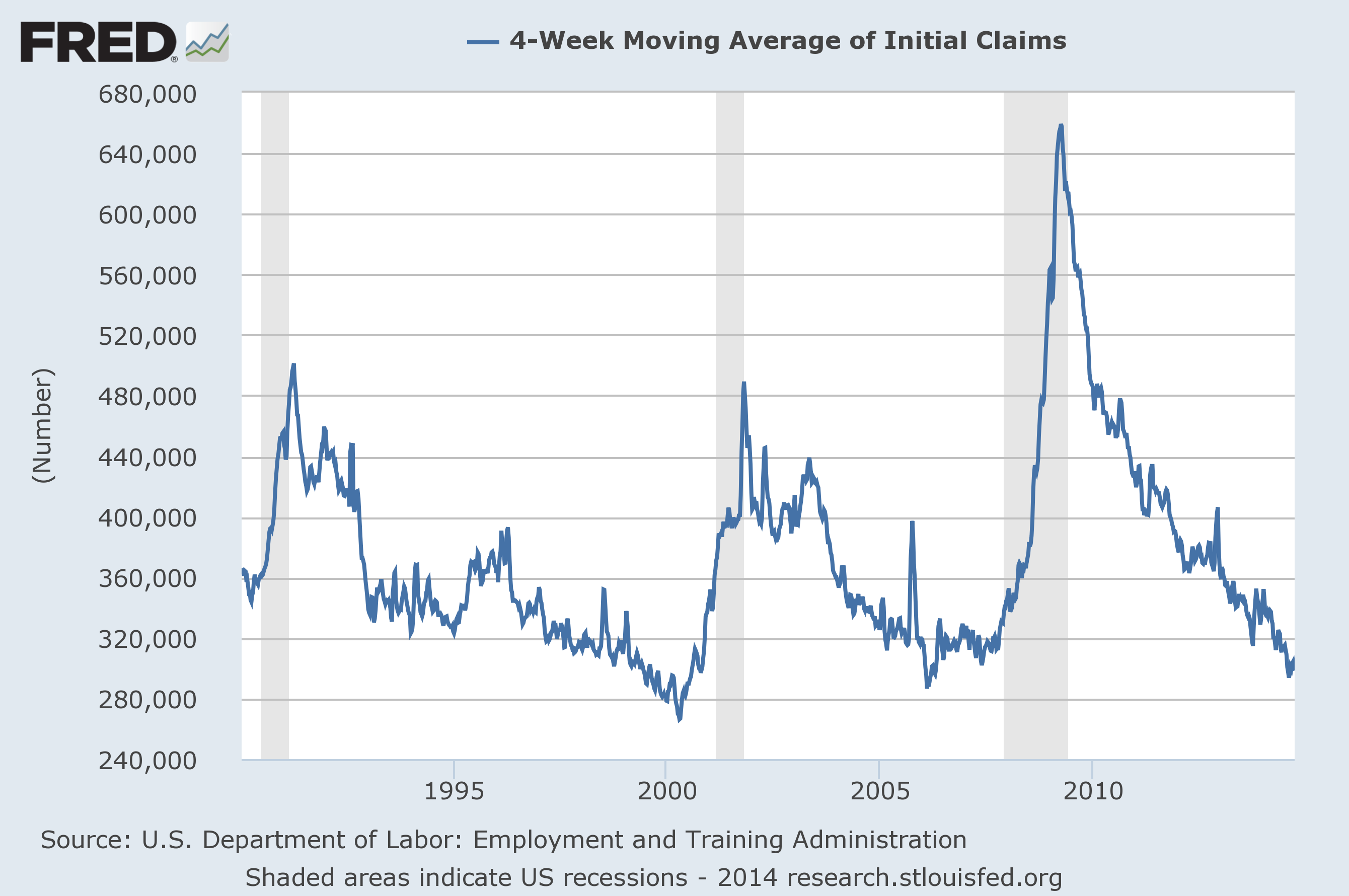

Labor data continues to improve, as the 4-week average of initial jobless claims has fallen to pre-recession levels:

And hourly average earnings are finally growing steadily, providing more support to consumer spending:

Given rising investment asset values and real estate prices, household net worth in the US has now far surpassed pre-recession highs:

And households have essentially fully deleveraged, now using the smallest percentage of household disposable income to make debt payments than any time in the last 35 years. This means more cash flow is available to households for current consumption, saving and productive investment:

Despite a setback during the first quarter, second quarter real US GDP growth was a very healthy 4.6%, assuaging concerns over a possible recession and reflecting a continued trend of quietly healthy economic activity:

Finally, inflation remains low, signaling that the economy is not in danger of “overheating” and giving central banks plenty of leash to continue an accommodating policy position.

Year-End Planning

The end of 2014 is rapidly approaching, and investors would be wise to make sure they are thinking about planning opportunities that need to be handled before December 31st. Here is a quick rundown of items to keep in mind:

- IRA owners over 70.5 and anyone holding an inherited IRA are required to make annual distributions before 12/31. These distributions can be taken with in-kind securities or as cash. As of early October, Congress has not reinstated the ability for those over 70.5 to make qualifying distributions directly to a charitable organization. There is a small possibility that this could still be reinstated after the November elections, but personally I would not hold my breath on that. Many of those so inclined (who are also itemizing deductions) can take the distribution and make an offsetting charitable donation to the same effect.

- Review tax-loss harvesting opportunities. Investors should do this throughout the year, but year-end can serve as a good reminder to get this done if you have been putting it off.

- Consider charitable contributions. Deductions for charitable contributions work on a calendar-year basis, so make sure those contributions are in before December 31st. Direct gifts of highly appreciated stock can be an effective way to maximize the value of your gift and your tax benefits. Investors considering a donor-advised fund should also make sure that paperwork is handled well before 12/31.

- Establish and fund (some) retirement plans. Certain retirement plans must be established before 12/31 to be effective, and certain contribution types must be made before 12/31 as well. New SIMPLE-IRA plans must be established before 10/31 to be eligible for 2014 contributions, and employee contributions must be made by 12/31. Individual 401(k)s must be opened and funded with employee contributions before 12/31 (employer contributions are allowed up to the tax filing deadline, generally 4/15).

- Roth IRA conversions from a Traditional IRA must be made before 12/31 to appear on your 2014 tax return.

- To be eligible for a state income tax deduction (where available), 529 plan contributions must be made before 12/31.