Market Overview

Markets had a rough ride to small gains in the first quarter. After a quick drop during January and the first half of February, the S&P 500 recovered during the following six weeks to post positive returns of 1.35%. Small cap stocks could not keep up in the recovery rally and were down for the quarter. After years of underperformance, Emerging Markets stocks actually outshone their US counterparts, posting very strong first quarter gains of 5.37% on the weakening US Dollar. This reversal also found its way to natural resources, with S&P 500 Energy sector stocks bouncing 4.02% during the quarter as oil prices (WTI) rose to over $39 after falling below $27 per barrel in January. Real Estate offered very strong returns as well with the S&P Dow Jones US REIT Index gaining 5.26% for the quarter. Bonds rallied as interest rates fell, with the Barclay’s Aggregate bond gaining 3.33% and the yield on the 10-Year Treasury fell to 1.78% from nearly 2.25% at the beginning of the year.

Economic Update

I sound like a broken record each quarter, but the US economy continues to move along at a slow but upward pace. 2015 full year real GDP was revised upwards in February to a rate of 2.4%. Certainly not exciting, but reasonably healthy, and mirroring the growth rate of 2014. This was in spite of a very strong dollar in 2015 that led to falling exports, offset by personal consumption and residential fixed investment.

While the US Dollar gained steadily in 2015, continuing a multi-year trend, it peaked in mid-January and has since fallen back to levels from mid-2015.

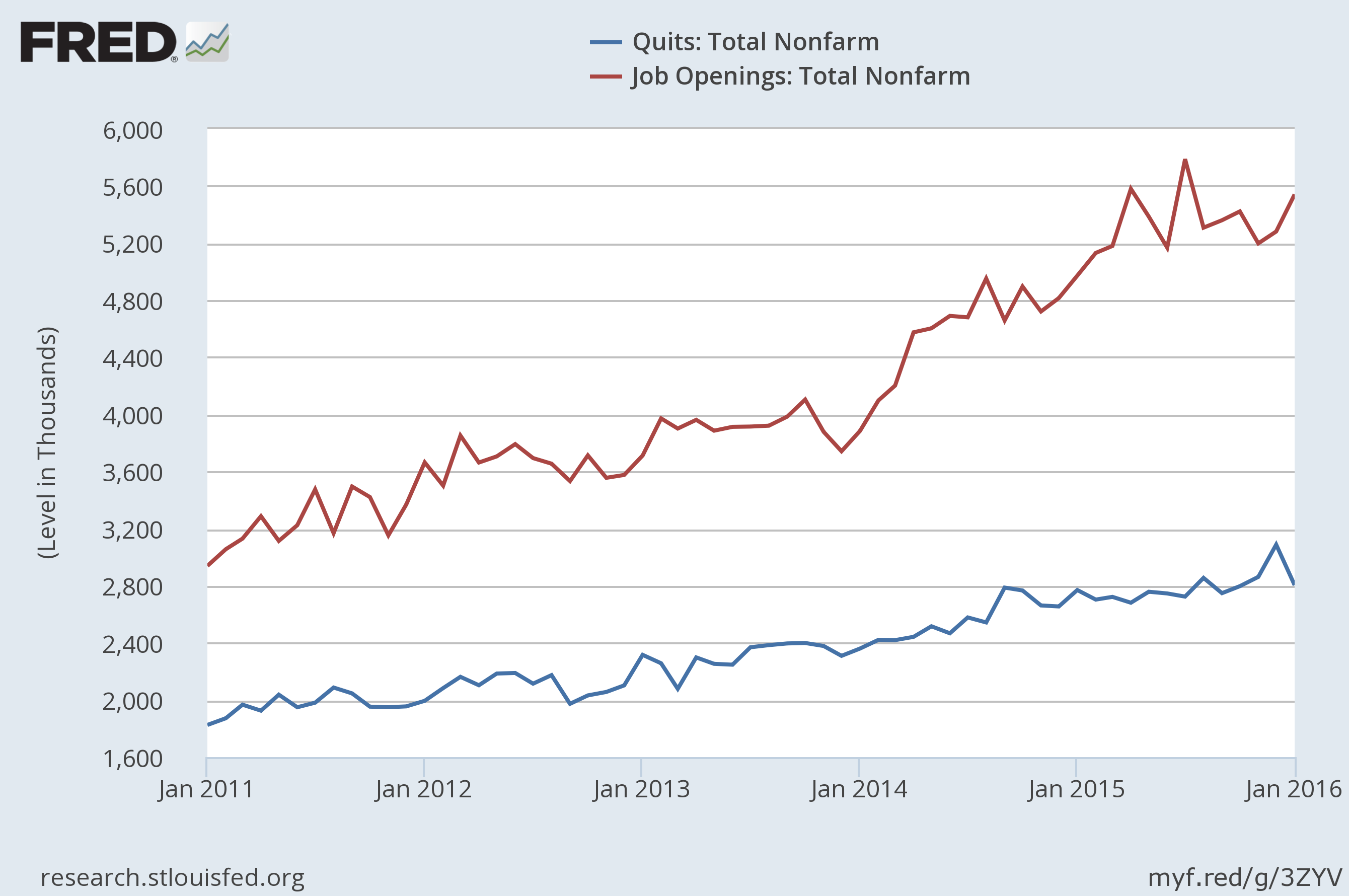

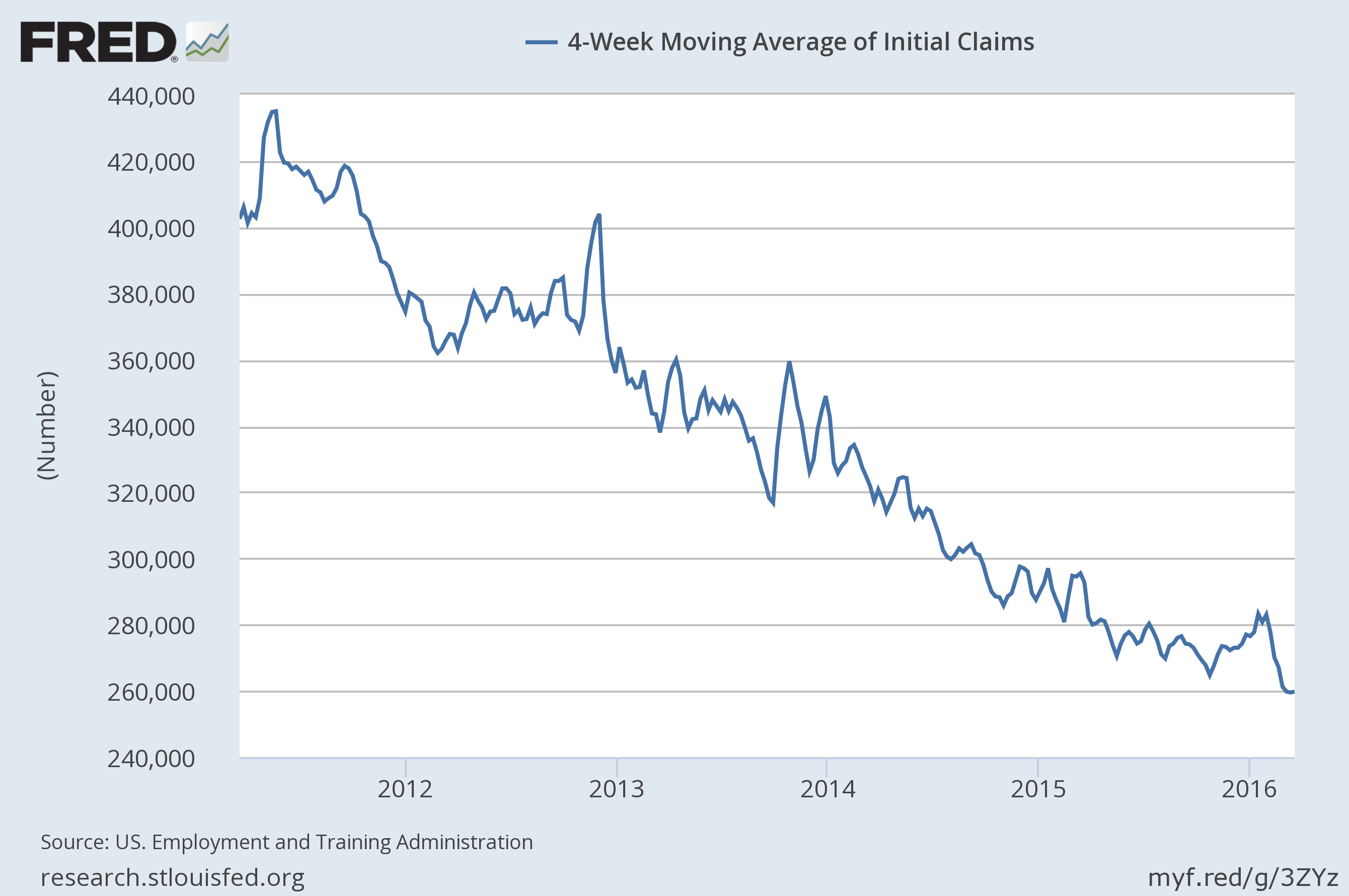

The US job market continues to improve for labor conditions as more and more jobs are opened, more individuals quit their jobs and fewer file for unemployment benefits. Unemployment has remained steadily low, and the workforce is expanding again as more workers re-enter in search of employment. The March jobs report beat expectations with 215,000 jobs added and the labor force participation rate gained, up to 63%. Hourly earnings gains also beat expectations, up 2.3% from a year ago.

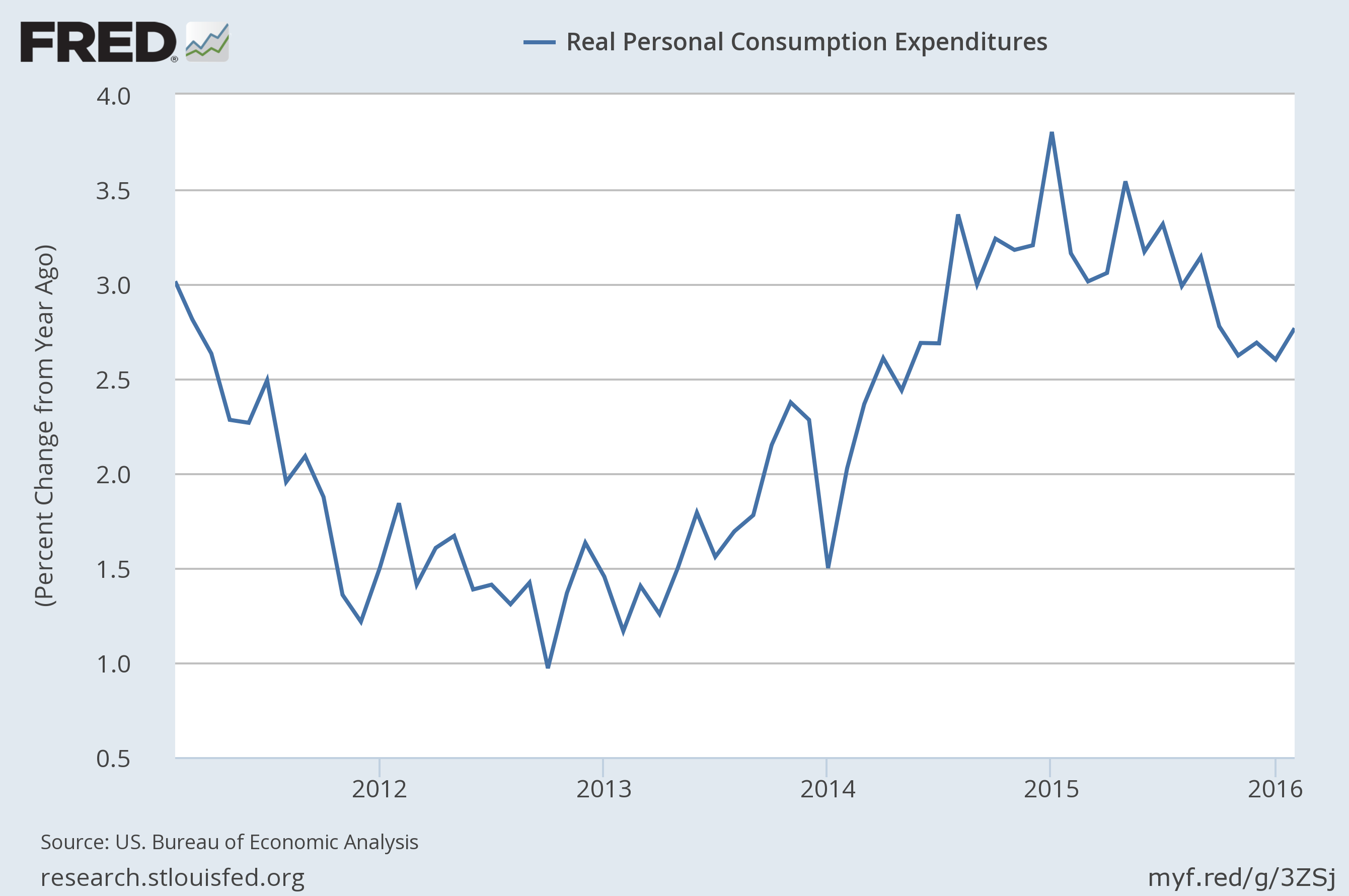

US consumer spending growth is still positive after inflation. This data is in keeping with the overall trend of a slow-growing, generally healthy US economy (that continues to be in the best shape it has been since the 2008 recession).

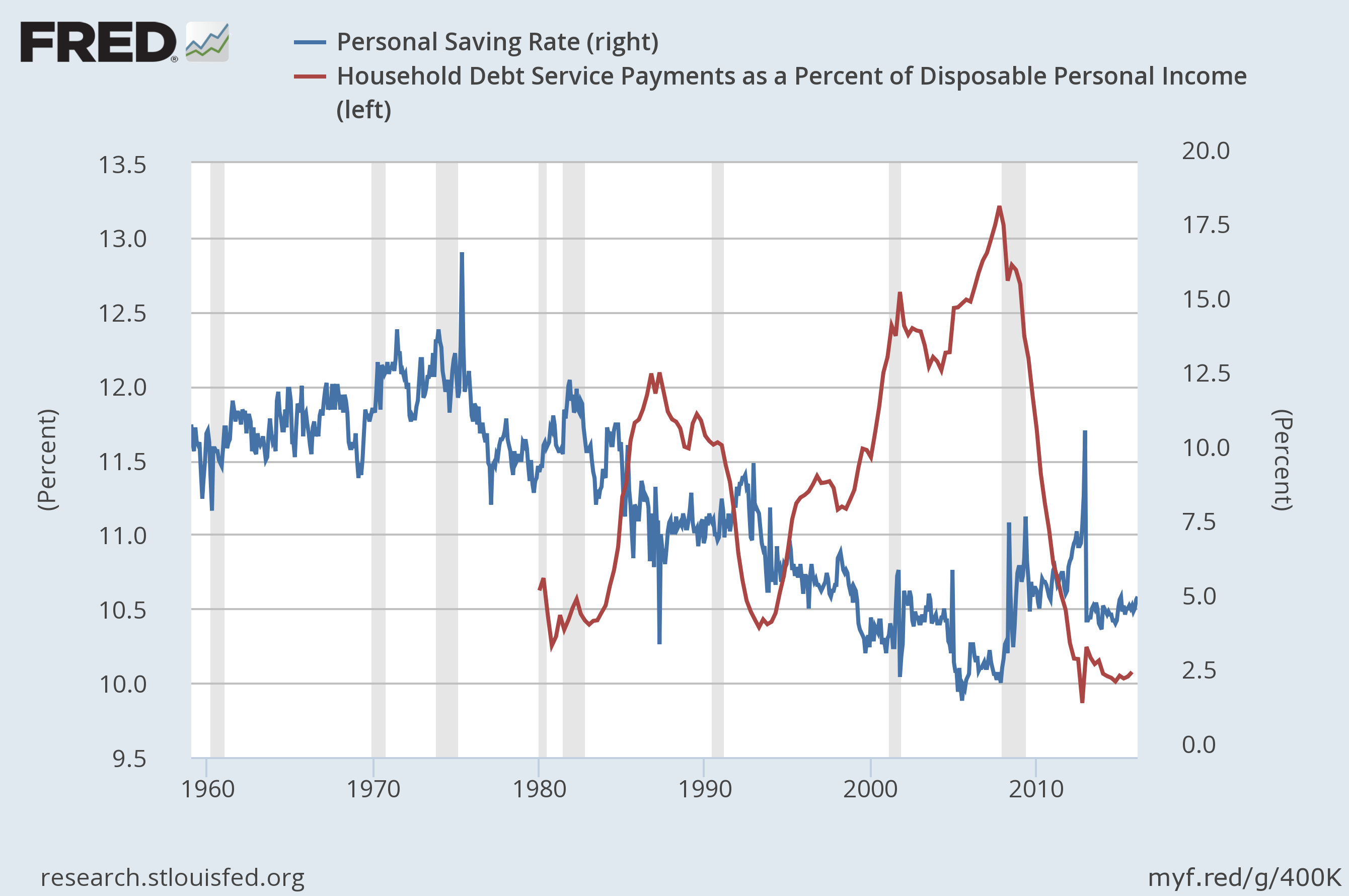

Households remain in remarkably good shape. Debt service ratios (how much of their disposable income individuals use to make debt payments) are at generational lows and the personal savings rate is very stable around 5%.

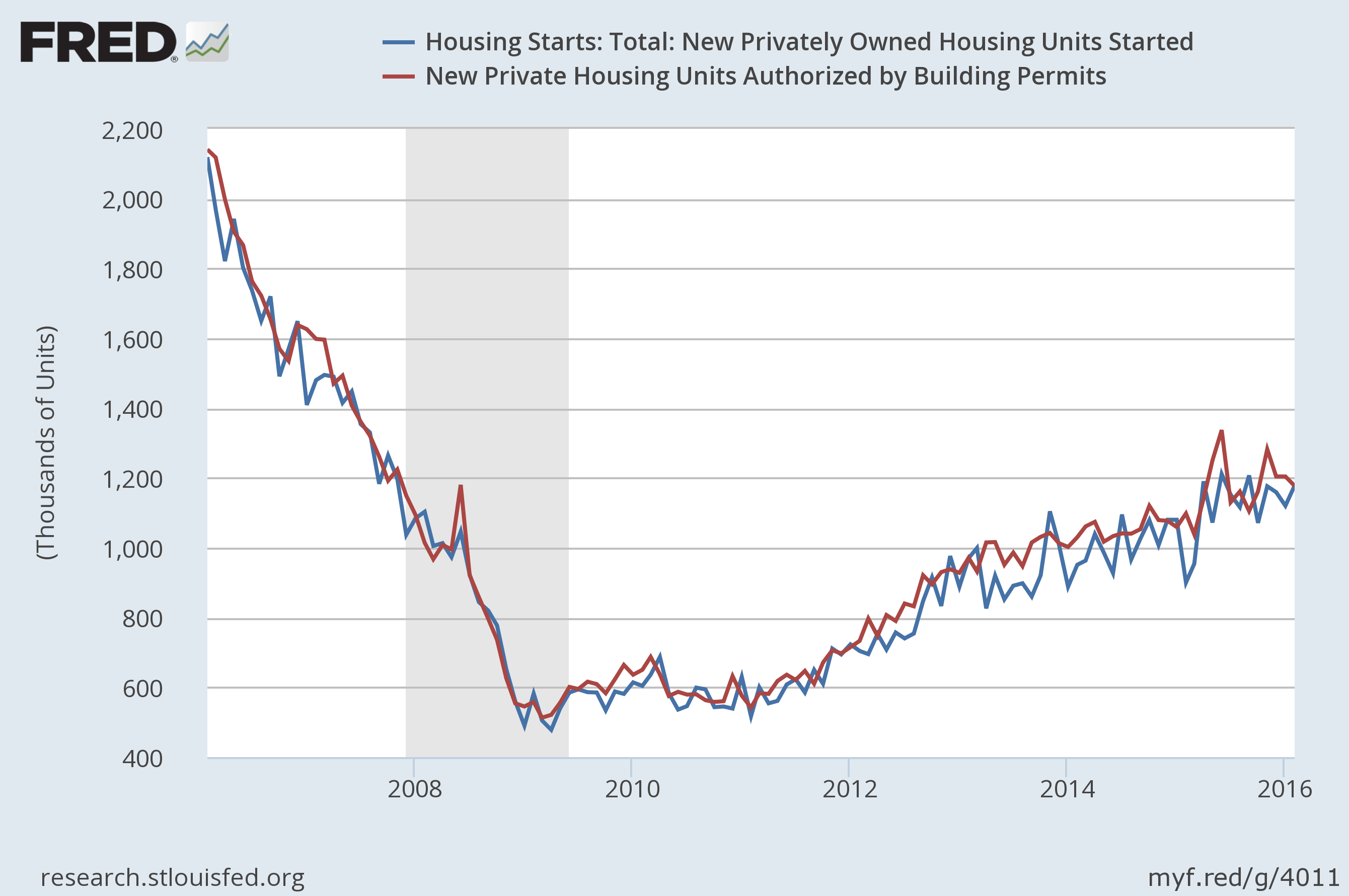

Finally, housing continues to show steady improvement, with residential starts in February growing at a 5.2% annualized rate. Permits and starts have tracked upwards nicely since the 2008 recession, showing their strongest annual growth over the last 12 months.

Tax & Legal Updates

While there was not significant legislation to come out of Washington this quarter, rumors were many. Most of these sprung from the President’s February budget recommendations. Of course, we are in an election year with a term-limited President and Congressional control under his opposite party, so not much is likely to happen this year.

However, the budget gives us a relatively brief glimpse of what politicians in DC might be considering in the future, depending on party control and willingness to compromise. Evidently these include the possible elimination of the “backdoor Roth IRA” strategy, new Required Minimum Distribution rules for Roth IRA owners over 70.5, and the potential elimination of the automatic step up in cost basis for inherited assets.

To this last point, the IRS is now requiring that executors of a personal estate file a new form (Form 8971) to report the cost basis of inherited assets along with Form 706 for estates. This ruling will apply to all estate returns filed after July 2015. It is possible, of course, that this ruling is a precursor to changes we may see in the future. The proposed elimination of cost-basis step up would require that beneficiaries treat all assets as liquidated upon death, realizing any exposed capital gains. This, of course, is mostly gossip at this point and would require an act of Congress to change existing estate tax laws.

Most of these proposed budget ideas have popped up in the past and gained no traction, and there is little reason to believe things would be different this time. Generally, the best stance to take when making planning assumptions about the future is the status quo – it does, after all, require Congress to write, vote on, pass and have the President sign into law nearly any material change to current tax code and regulations.

As always, you know where to find me if you’d like to discuss any of these topics and how they apply to your personal situation.