Market Overview

Brexit Brexit Brexit Brexit Brexit. Heard enough yet? Yes, on Thursday June 23rd the voters in the UK elected to advise their government to leave the European Union, to the surprised of many. The markets reactive wildly, with big drops in global stocks on Friday and Monday. US stock markets recovered Tuesday and Wednesday, making up most of the drop, but it is still all we seem able to talk about. Before all of this, there was actually a quarter in the markets.

Depsite all the action, US stocks were nicely positive for the second quarter, with the S&P 500 returning 2.46%. Small caps (Russell 2000) fared even better with gains of 3.79%. International stocks were weak again, falling -1.46% for the quarter.

Bonds again gained as interest rates fell for another quarter. Over the last three months the Barclays Aggregate Bond was up 2.21% and is up 6.00% for the last year through 6/30/16. Municipal bonds also did very well, up 2.61% for the last three months and 7.65% for the last year.

Economic Update

More of the same, that’s what I’m here to tell you. First quarter GDP growth was revised upward in May to a benign 1.1% annualized. This is obviously low, but in line with the recent trend of slow first quarter growth in the last several years. If that trend holds, growth would pick up into the year. Early indicators based on current data show that we could reasonably expect second quarter growth to be more normal at 2.5% – 3%.

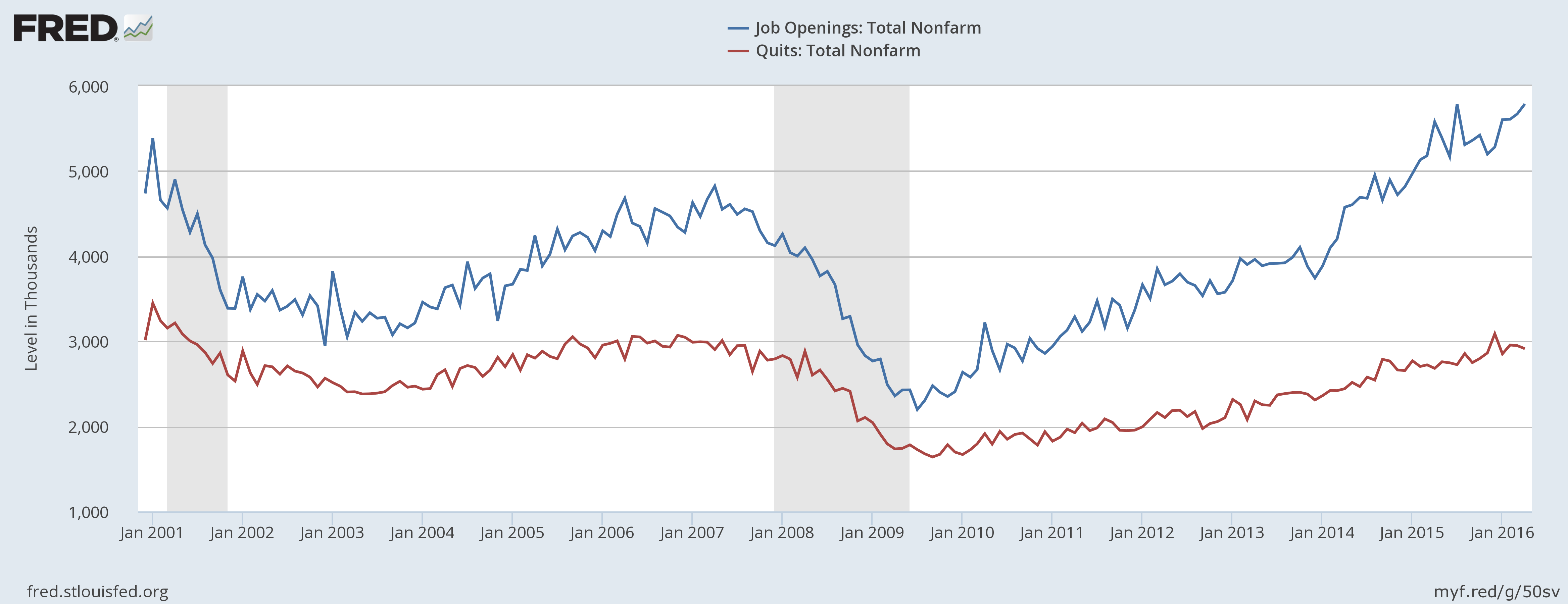

The official unemployment rate in the US fell to 4.7% in May after a very sluggish 58,000 new jobs added, largely due to a workforce that shrunk over the month. We’re seeing some typical signs of late-cycle economic activity – modest hiring growth, a job market inching closer to full employment, more upward pressure on wages and fewer applicants available for job openings. Below you can see that job openings are rising faster than people quitting their jobs, reducing the available pool of labor and driving up wages.

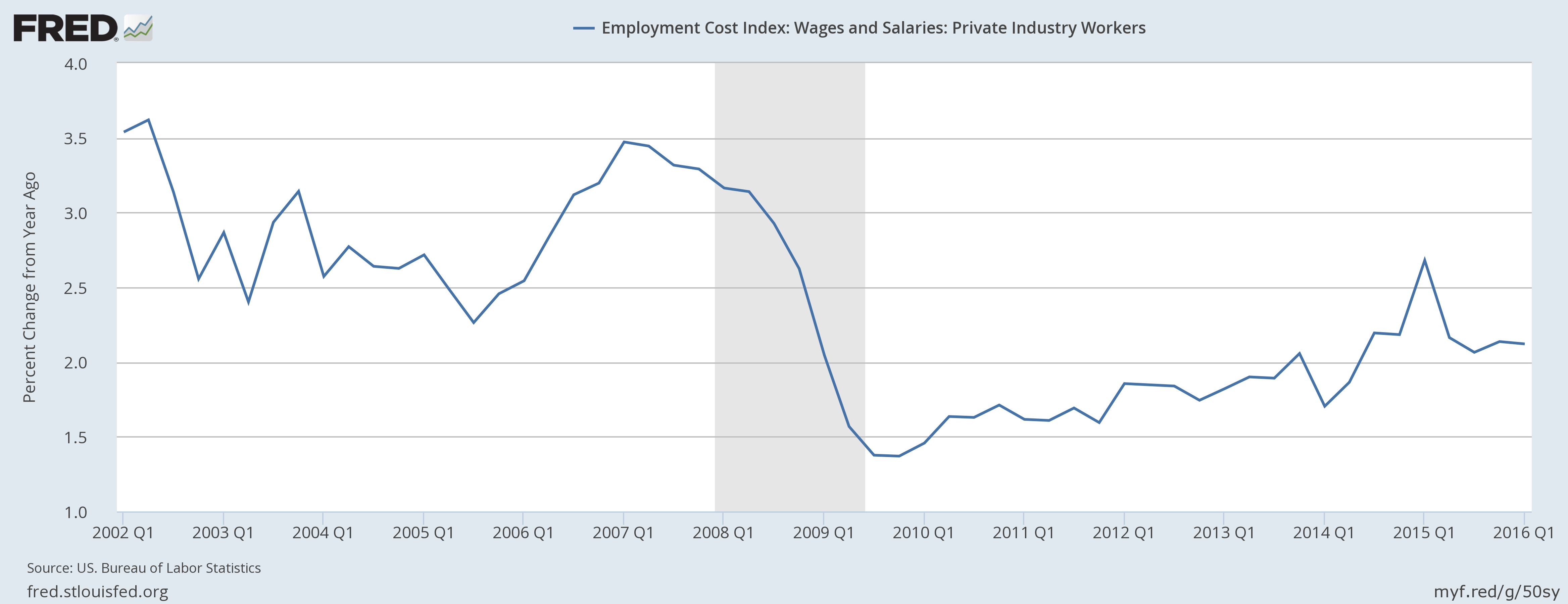

The employment cost index continues to tick modestly higher as private sector wages grow faster than inflation. Average hourly earnings also gained 2.5% year over year through May.

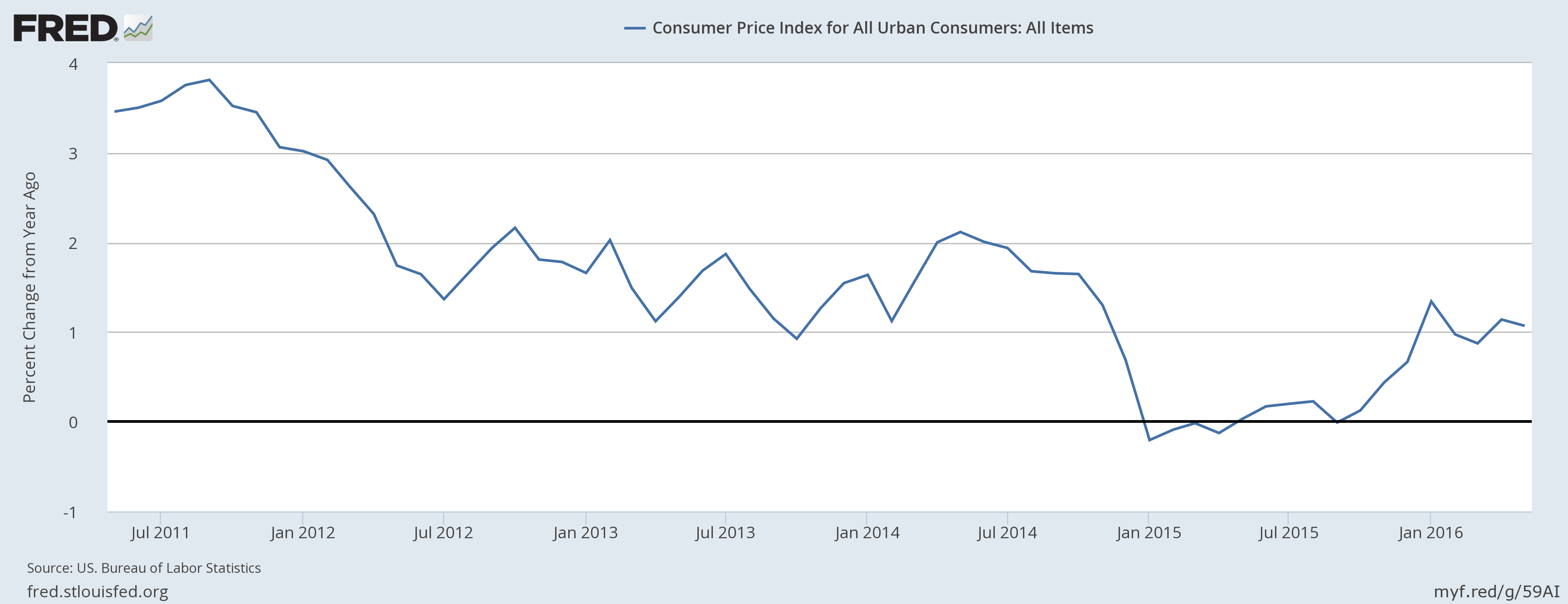

Inflation, in fairness, is a low hurdle to clear. The Consumer Price Index was up only 1.0% over the last twelve months (through May) as inflation remains subdued.

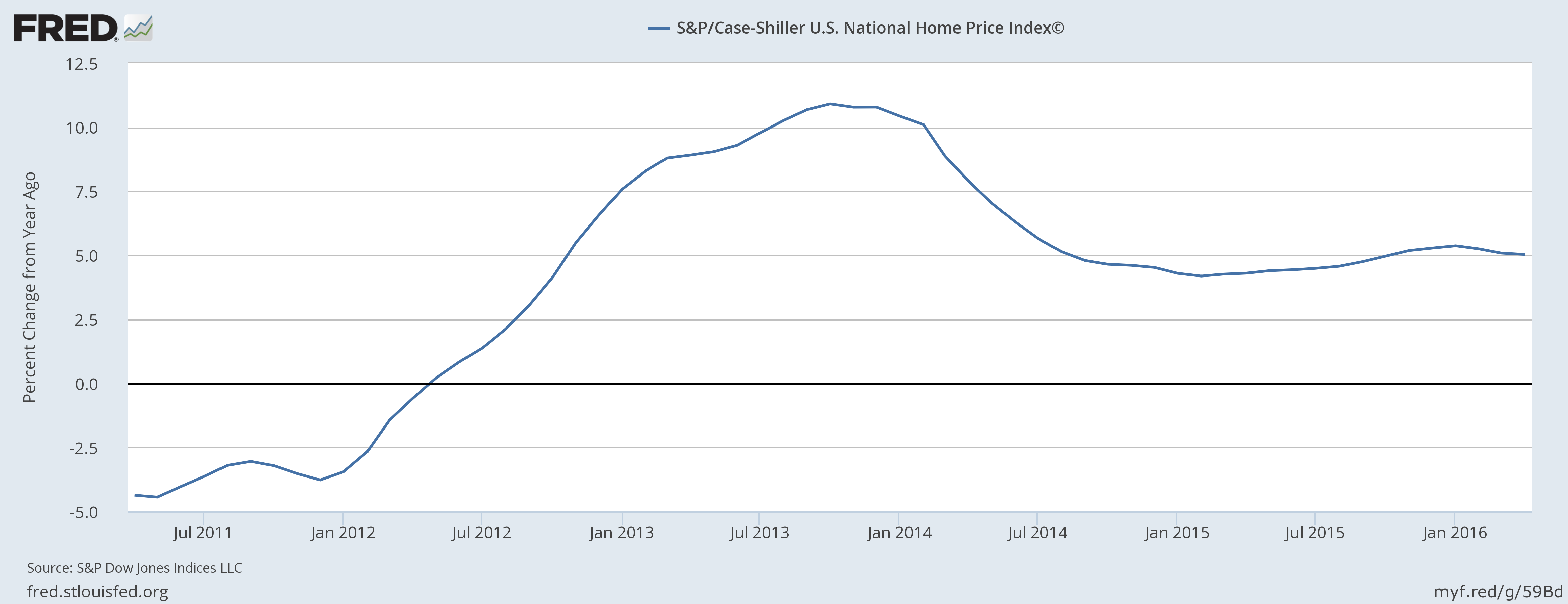

Real estate, often the biggest driver of US economic activity, is healthy and showing few signs of slowing. Locally, Denver home prices were up 9.5% year over year through April, and on average national home prices rose over 5% in the last year as demand continues to outstrip supply.

While this real estate and construction spending cycle was much slower to rebound than in a typical recovery, we’re seeing all healthy signs of growth as construction spending and employment grow to catch up with unmet demand for new housing. As the millennial generation finally starts to increase household formation and more of that population approaches typical first-time-homebuying ages, it is reasonable to consider that this trend may be sustainable.

In sum, rumors of a recession looming are probably overdone, but growth isn’t exciting. I think that’s roughly the 10th quarter in a row I’ve written that? I’ll be wrong eventually as recessions are an inevitable part of the cycle, and I’m not basing any kind of investment decision on my ability to predict such events. My goal is to moderate fear (and greed) when it comes to markets and the economy, and remind all of us that we’re poor predictors of future events, so we should probably ignore most of the above information and stick to a reasonable long term plan.

Tax & Legal Updates

The big news out of Washington as it affects the world of finance is the Department of Labor’s passing of the Fiduciary Rule on April 6th, 2016. After much back-and-forth with the industry, rulemakers came to a final, enforceable statement. Effective June 7th (alongside some longer term phase-ins), all advice given to investors under DOL covered accounts (generally speaking, IRA rollovers and 401(k) retirement plans) must meed a fiduciary standard. The DOL is attempting to curb abusive practices in retirement savings vehicles, including conflicted advice, inappropriate products and forced arbitration. The Fiduciary Rule is a best-interests standard, a much higher standard than the typical “suitability” most brokerage houses currently abide by.

So what does all this mean? Thanks to lots of available exemptions, many practices will continue, including the sale of commissioned and proprietary products. The most meaningful impact is that the Fiduciary Rule gives investors real recourse and the ability to sue providers in open court. For many of us professionals who have already (and voluntarily) been held to a fiduciary standard, there aren’t major changes. I’ve always been able to be sued in open court and when this firm was Colorado-registered (now SEC-registered), the state explicitly prohibited “binding arbitration” clauses in client contracts.

Of course, the securities industry is already fighting back against the rule, claiming that providing best-interests advice will somehow be prohibitively expensive, and is heavily lobbying congressional representatives to attempt to overturn the rule. This isn’t likely to amount to much of anything and the consensus is that the rule is here to stay, at least for retirement accounts. Note that this rule does not cover non-retirement assets, where brokers remain free to sell shoddy products to unsuspecting investors.

The last news is that after being passed at the end of 2014 with the “tax extenders” legislation, newly created 529 ABLE accounts are beginning to pop up in some states as they are rolled out one by one. Colorado is shooting for 2017 to offer these, but some states with existing 529 plans are starting to roll out 529ABLE accounts. Designed to provide tax benefits for the needs of disabled individuals, 529ABLE accounts function in many similar ways to 529 education plans, including some offering in-state tax deductions or credits for contributions. Funds can be withdrawn tax-free for qualifying expenses including medical treatment, education, transportation, assistive technology and housing for the disabled beneficiary. 529ABLE accounts also provide an asset exclusion for the first $100,000 to avoid negative impact of eligibility for other Federal aid including Medicaid and Supplemental Security Income.

Contributions to a 529ABLE account are limited to the same annual gift limit as standard 529 accounts and are restricted to one account for each beneficiary. Eligible individuals must have a signed physician’s diagnosis of their disability to prove eligibility for the ABLE account. More information from the IRS regarding benefits and restrictions is available at this link.

As always, you know where to find me if you’d like to discuss any of these topics and how they apply to your personal situation.