Market Overview

It’s almost hard to remember that a little more than 3 months ago we were all on the edge of our seats with much hand-wringing over the potential fallout of Great Britain voting to leave the EU. But, as these things tend to do, the apparent crisis faded away as the initial over-reaction calmed down and life moved on. Instead of panic, the markets spent the summer in a quiet period of very nice gains, with little volatility despite Brexit and a US Presidential election cycle we’re all desperately hoping will be over soon.

US stocks both large and small had a remarkably good quarter. Large caps as represented by the S&P 500 gained a solid 3.85% over the last three months, and were handily outpaced by small caps (Russell 2000) which were up 9.05%. This appears to be a reversal of a long trend of large cap stocks leading the way, but time will tell what comes next.

International stocks also had a strong quarter, with the MSCI EAFE benchmark gaining 6.43% after years of struggling to keep pace with US markets. Much-beaten down emerging markets also had an impressive three months, posting gains of 8.32%, ahead of their developed-market peers.

Finally, once again, the bond market remains steady with a largely flat quarter from the Barclays US Aggregate Bond index returning 0.46%. Corporate bonds fared slightly better than US Treasuries at 1.49%, and municipal bonds were slightly negative at -0.30% over the last three months.

Economic Update

Despite what some public figures with an axe to grind may have to say, the US economy is doing just fine, thank you. Perhaps even better than fine, perhaps it is doing pretty well! Jobs, employment, earnings, real estate values, household balance sheets, inflation, financial assets, you choose how you want to measure things – it is hard to make a strong argument that the economy has been anything but solid. Not exciting, not on fire, but solid.

First, work. Job openings in the US reached an all-time high in July of 5.87 million. That’s 5.87 million available jobs, employers looking for qualified people, ready to pay them. Another 2.98 million people voluntarily quit their jobs in June, a sign of confidence in the job market – people who are worried about finding a new job typically don’t quit their existing one. The ratio of job seekers to job openings fell to 1.3, the lowest measurement since 2001. These measures are generally indicative of something like full employment, often signaling that increased wages could be around the corner.

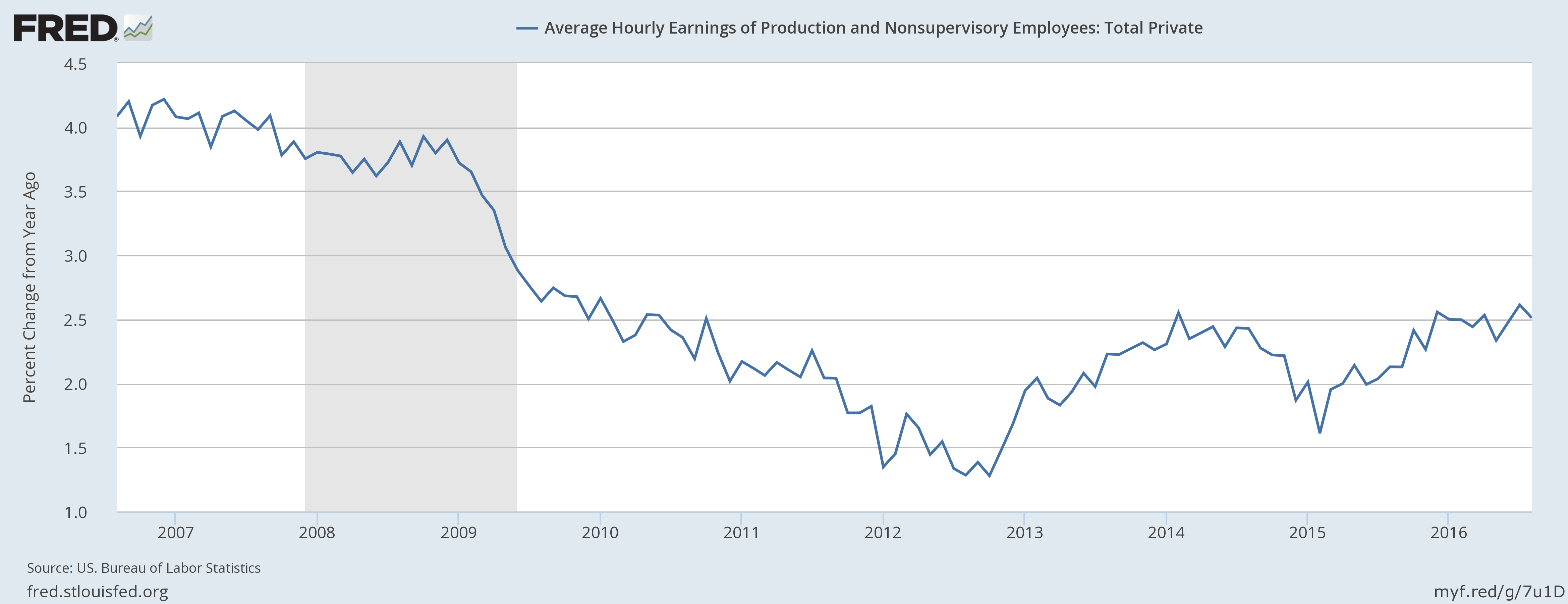

And speaking of wages, the census bureau reported that in 2015 median household income jumped 5.2%, the first annual increase in 8 years and the largest single-year increase since 1967 when these figures were first tracked. And while not overly exciting and certainly lower than post-recession levels, the annualized growth in hourly earnings for most workers has been trending up over the last few years.

Nationwide, residential real estate prices are rising with the Case-Shiller US National Home Price Index up 5.1% in July over a year before.

In other signs of a very healthy US consumer, Vehicle Miles Traveled in the United States continues to hit all-time highs, in part thanks to ongoing low gasoline prices.

Real personal spending (Personal Expenditures) continues to grow at rates above inflation:

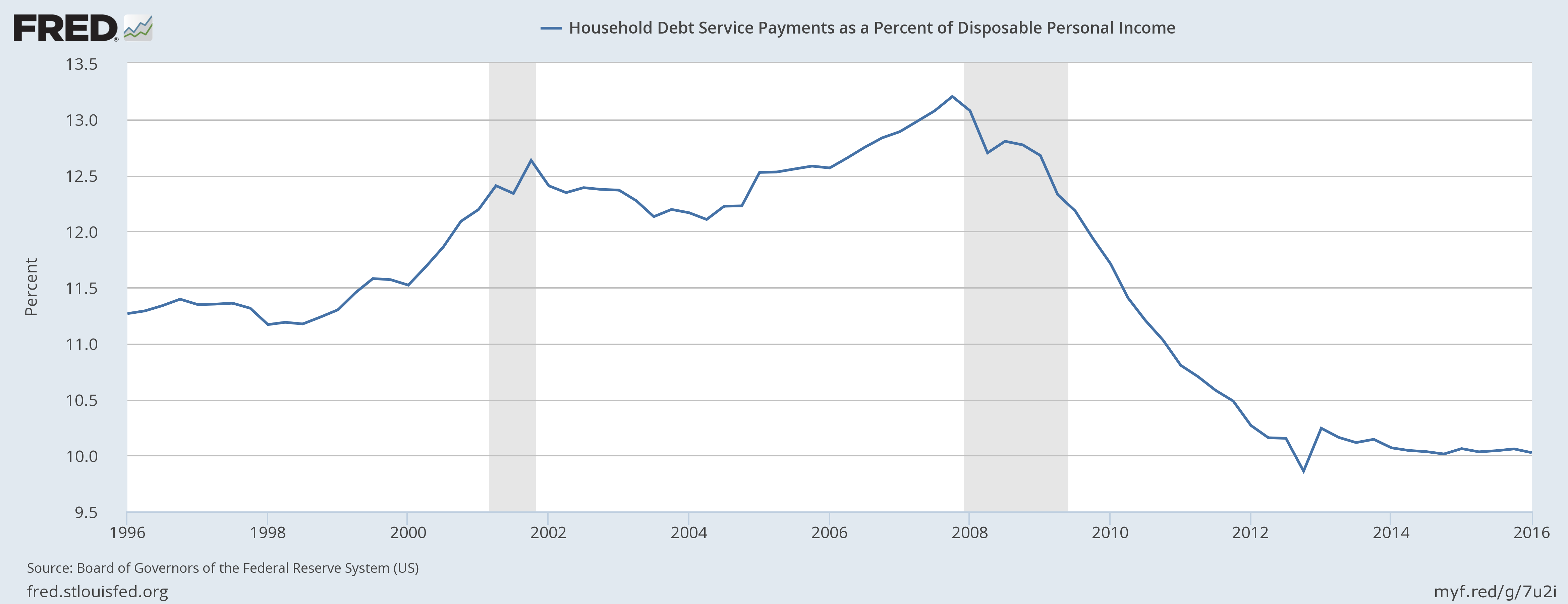

While households continue to spend a very small portion of disposable income on debt payments and household balance sheets grow to new highs.

Despite these economic gains, inflation remains subdued at just 1.1% through August. As this remains well below the Federal Reserve’s target rate of 2%, the Board again voted in September to defer another rate increase, while leaving the door open for speculation about an increase at this December’s meeting.

Tax & Legal Updates

I must be getting older, because the years are going faster. And here we are again facing the end of a calendar year, which means it is time to make sure we are thinking about tax planning before the clock turns over to 2017 and many opportunities are lost. So here is a quick rundown of things that we need to make sure are done before December 31st.

- Deductible 529 contributions to most state plans (including Colorado).

- Charitable gifts for the 2016 tax year, including in-kind gifts of stock or mutual funds.

- Required Minimum Distributions from IRAs, former employer retirement plans and inherited IRAs. Don’t forget that direct gifts to charity can still be used to satisfy RMD rules, and this is now permanent. Well, as permanent as anything out of Washington D.C. can be.

- Available tax losses to harvest.

- IRA to Roth IRA conversions.

Additionally, open enrollment for individual health care policies begins November 1st. If (like me) you carry a private health insurance policy outside of your employment or Medicare, it’s time to review and possibly renew or replace that coverage. Open enrollment for 2017 ends January 31st, 2017, and policies must be purchased by 12/15/16 to be in place by 1/1/2017.

As always, you know where to find me if you’d like to discuss any of these topics and how they apply to your personal situation.