Market Overview

The rally that began shortly after last November’s election continued early this year, with US large cap stocks yet again posting a very strong quarter, up over 6%. International stocks fared even better, including Emerging Market stocks really turning a corner after years of significantly underperforming the S&P 500; up 11.14% for the quarter. Emerging Market currencies have gained on the US Dollar year to date, further boosting returns for US investors in emerging markets. Bond returns were flat, despite continuous fears of rising rates, as the 10-year Treasury has remained largely unchanged. My takeaway remains the same: there’s no predicting what comes next. Markets and asset classes turn on a whim and we won’t ever accurately predict when and to what degree. We’ll have gains when the markets offer them and rebalance into underperforming asset classes as dictated by our investment policy statements. All else is madness!

Economic Update

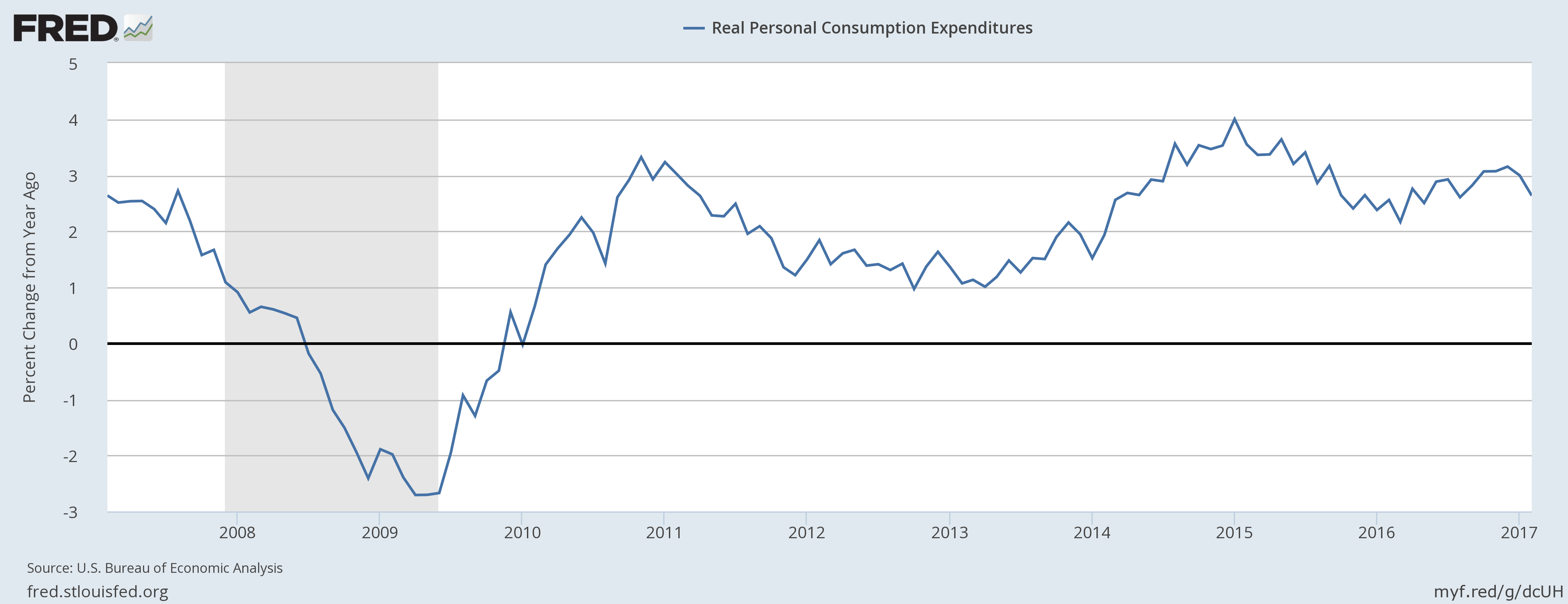

What’s new in the economy? Not a whole lot. Fourth quarter Gross Domestic Product was revised slightly higher in March to 2.1%, down from the 3.5% year-over-year change in the third quarter. The fourth quarter brought full year economic growth up to just 1.6%, a lackluster result and the worst year since 2011. Growth in real personal spending remains positive, although slightly down from its recent peak rate.

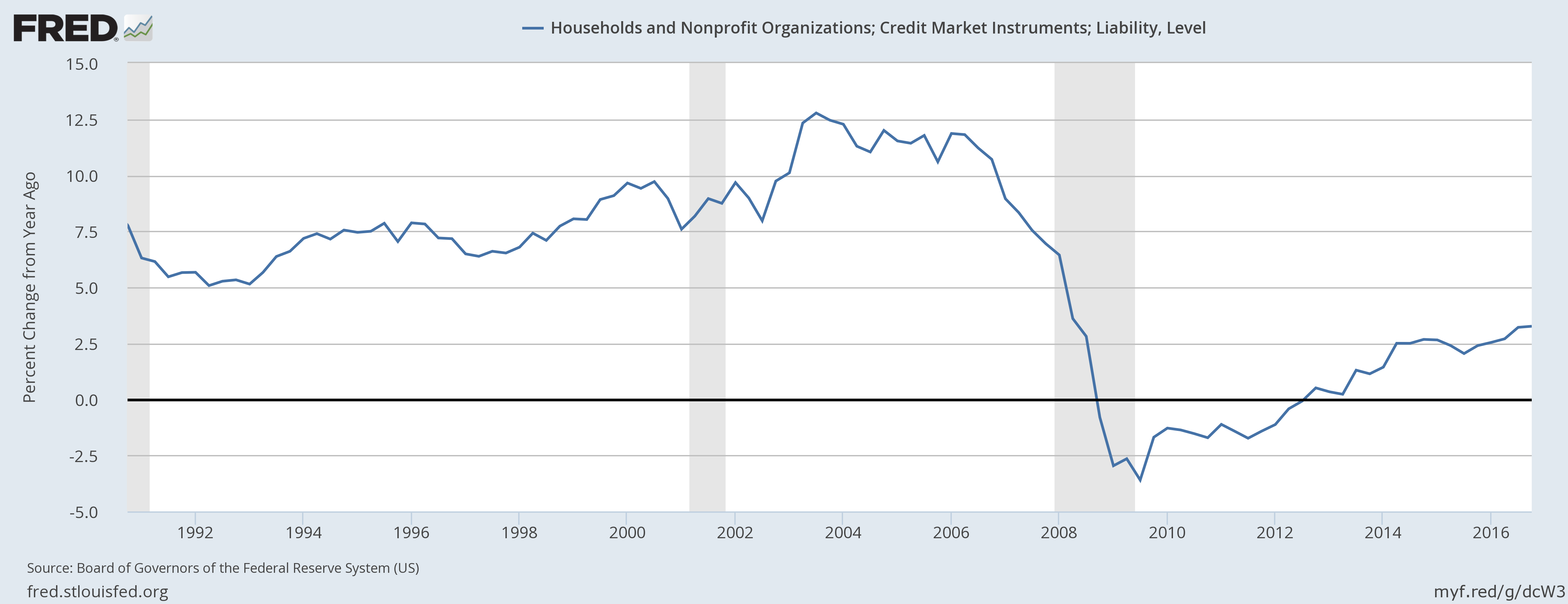

The pace of borrowing from households has simply not come close to resuming its previous growth rate. For nearly two decades before the recession, liabilities grew at 5-10% per year steadily. Even now, 9 years out from the recession, we’re now only just above 2.5% annual growth in debt.

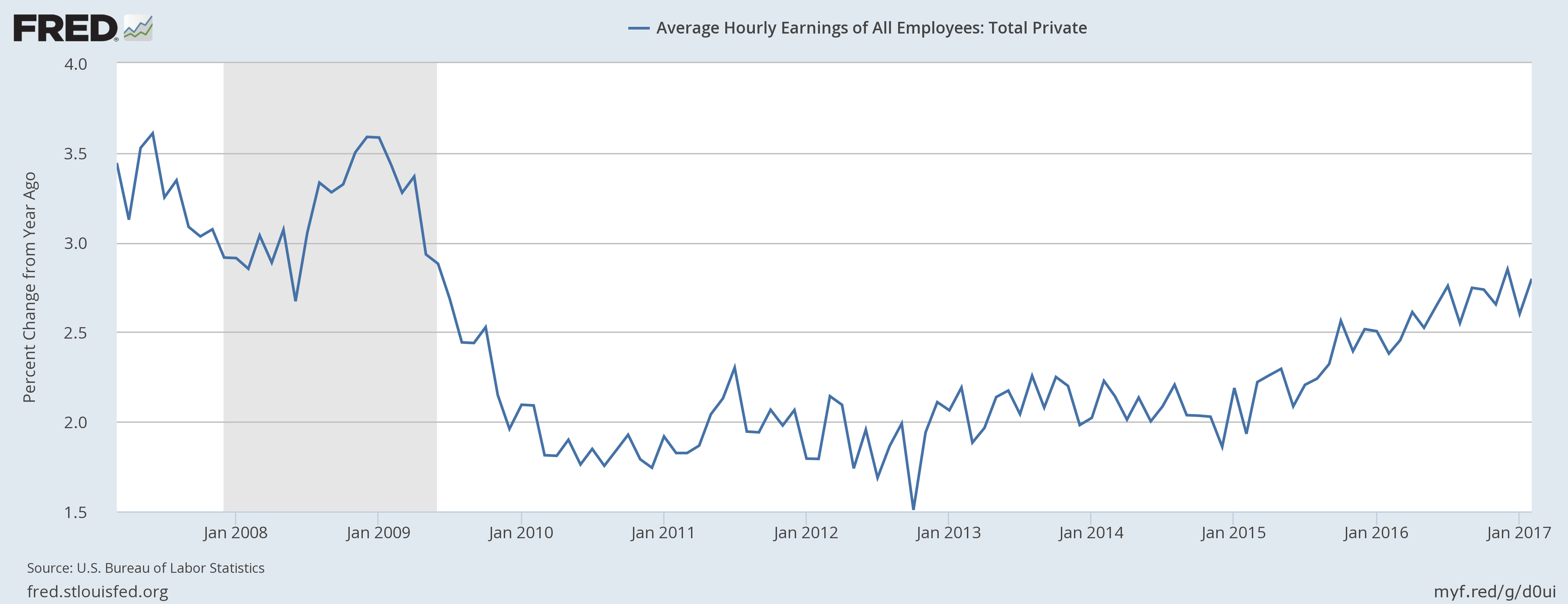

As we could expect in the latter half of an economic cycle, wage growth has been slowly ticking up over the past few years, putting the average worker on better financial footing.

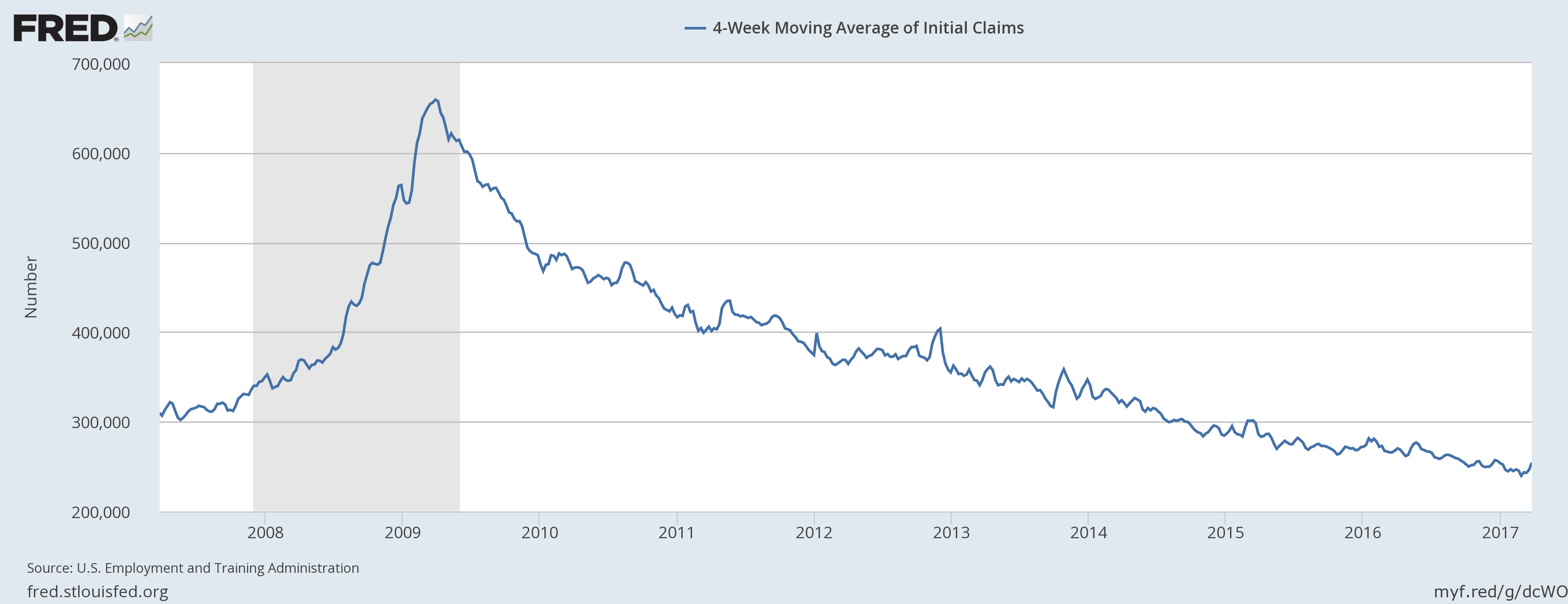

This coincides with steadily falling initial jobless claims as the labor market is as robust as it has been in years, and well-below pre-recession levels.

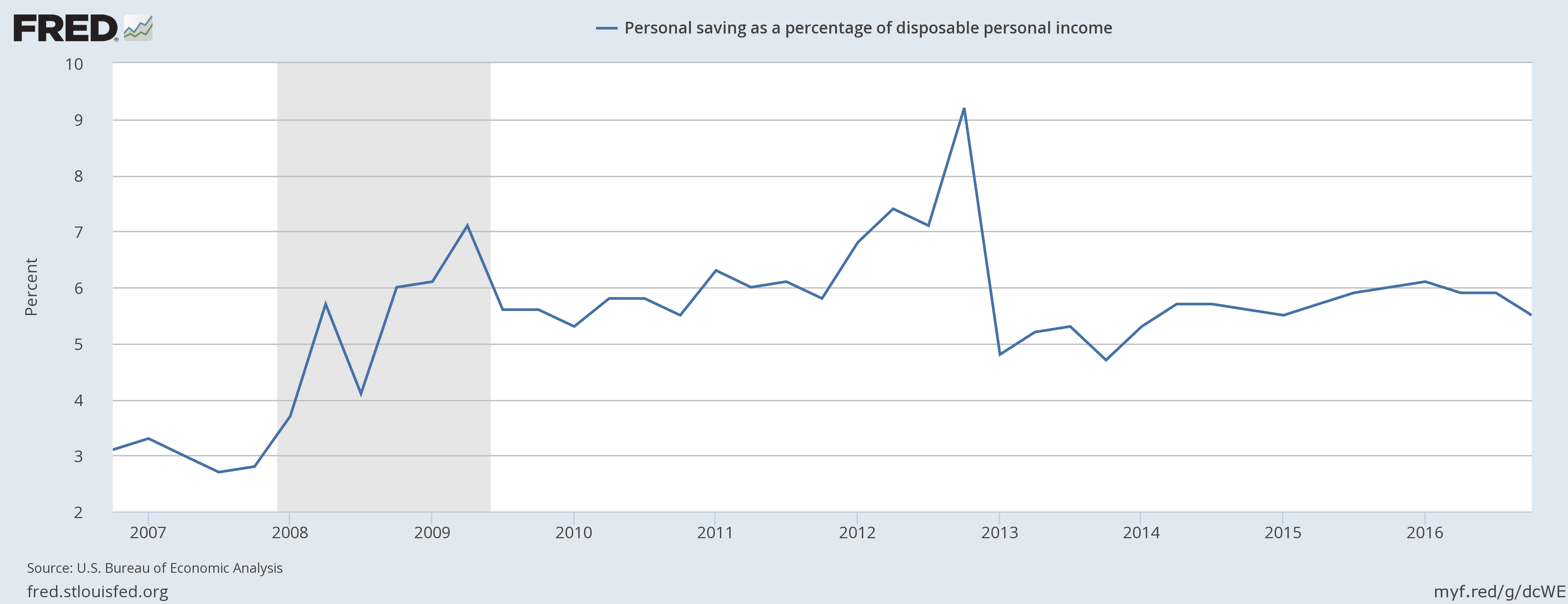

The personal savings rate in the United States has remained steady and reasonably healthy.

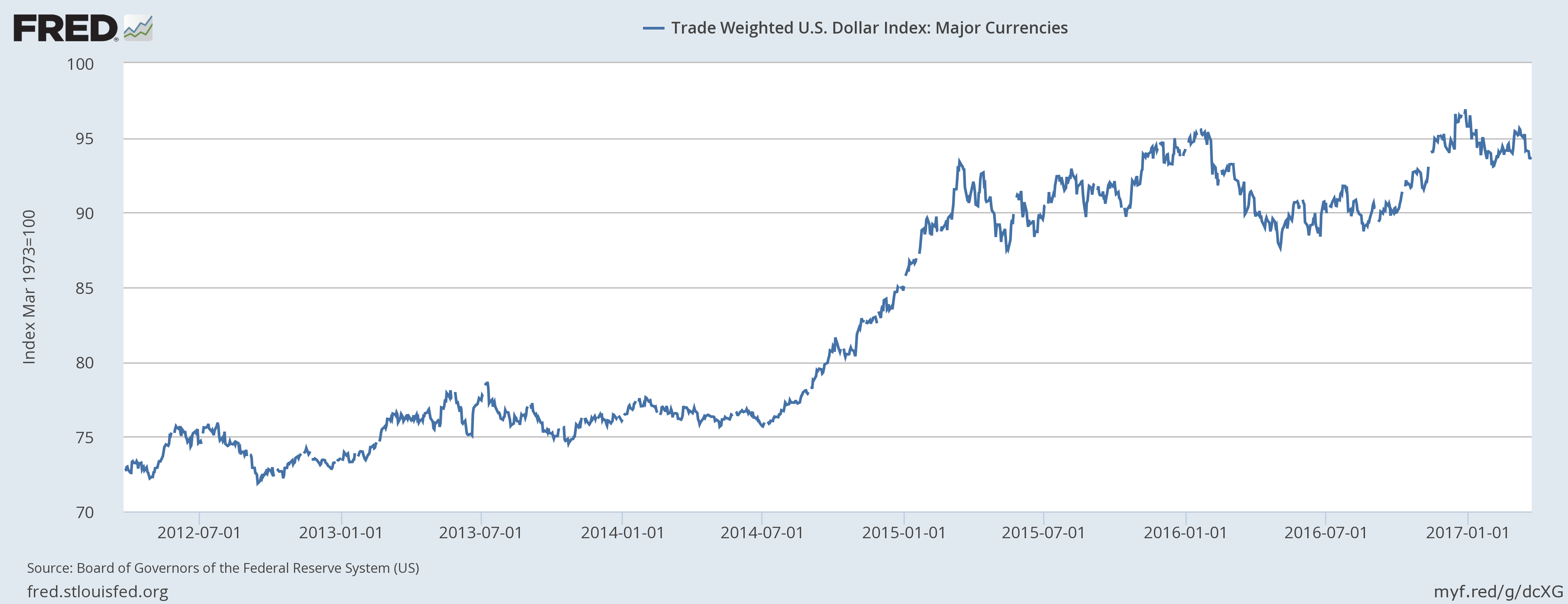

As mentioned above, the US Dollar has slowed its long term trend, peaking in late 2016. While we cannot know what happens next, what we’ve seen year to date is that this relative weakening in the Dollar relative to other currencies has been a boost to international investments for US investors.

Tax and Legislative Updates

Despite Republican majorities in both congressional houses and a sitting Republican president, we’ve seen little legislative impact to date. Republican plans to replace the Affordable Care Act (aka Obamacare) fell flat as house speaker Paul Ryan pulled the bill (the American Health Care Act) shortly before a scheduled vote after it became apparent the bill lacked support to get out of the House. According to Speaker Ryan as of late March, repealing the ACA will not continue to be a near-term legislative priority.

While it seems likely that tax reform would be the next priority, it is unclear how much consensus currently exists among various arms of the Republican party to get significant legislation passed. Because of the slim 51 vote majority in the Senate, a full bill requiring 60 votes is unlikely, and the more limited reconciliation process is probably the only way to get a legislative change passed in this environment.

President Trump also released his proposed budget in March. As expected, the proposal included large cuts to nearly all non-military discretionary programs alongside a $50 Billion increase in defense spending. Left out of the budget were President Trump’s announced plans for a $1 Trillion infrastructure spending program, details of which are allegedly forthcoming later this year.

It’s important to remember that a sitting president’s proposed budget is just that – a proposal. It is an advisory document at most. Ultimately Congress must define and pass a federal budget (or, as has been the case recently, operate under a continuing resolution without an officially passed new comprehensive federal budget).

If we’ve learned anything over the past 8 years, it is that it is really, really hard to get things done in Washington. Even with single party control over the White House, House and Senate, coming to consensus on spending, legislative and tax priorities may be harder than it once appeared. We may see tax reform this year or next, but trying to plan around such speculation is risky business. We can debate whether this fact is a feature or a bug, but for planning purposes, it is often best to assume the status quo.