Market Overview

It has been another solid, steady quarter in the markets since the end of March. US stocks both large and small posted strong positive gains of 3.09% and 2.46% respectively. Tech continued to dominate with the Nasdaq posting gains of 3.87% over the last 3 months.

Broad bond benchmarks were also again positive recently with the Barclays’ Aggregate Bond up 1.45% for the quarter but off slightly -0.31% for the last twelve months ending 6/30/17. Municipal bonds (via the Barclay’s Municipal Index) also gained 1.96% for the quarter. Longer term bonds with more interest rate exposure performed best as long-term rates declined and the yield curve flattened.

International stocks had a great quarter, with developed economies (MSCI EAFE) gaining 6.36% over the quarter and 22.20% over the last twelve months ending 6/30/17. Emerging markets were also positive for the quarter, up 4.34%.

Economic Update

US economic trends remain relatively unchanged over the last quarter. Unemployment is low and job gains have moderated. The Bureau of Labor Statistics reported that in May the domestic economy added 138,000 jobs, dropping the unemployment rate modestly to 4.3%, the lowest level since 2001. Over twelve months ending in May, 2.23 million jobs were added, a solid if not exciting figure.

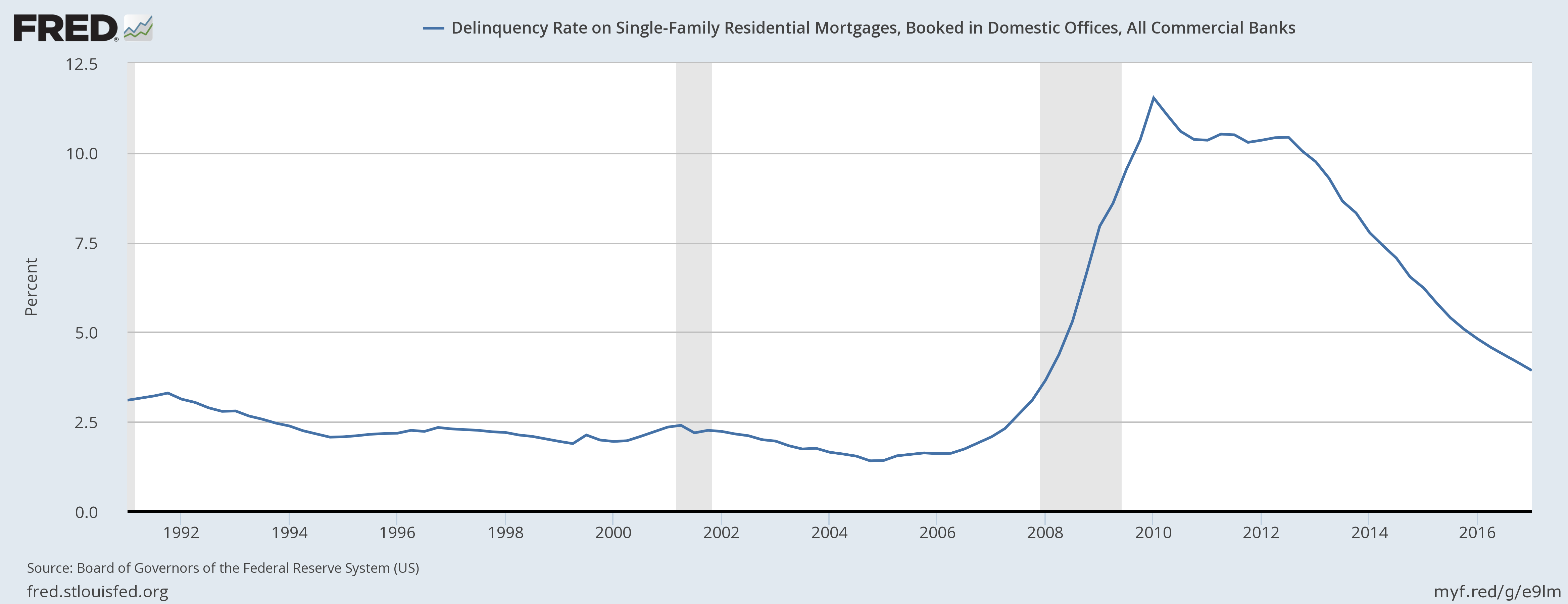

Aided by low mortgage rates and a healthy economy, mortgage delinquency rates continue to fall. Although still higher than pre-2007 levels, we are slowly approaching historical averages.

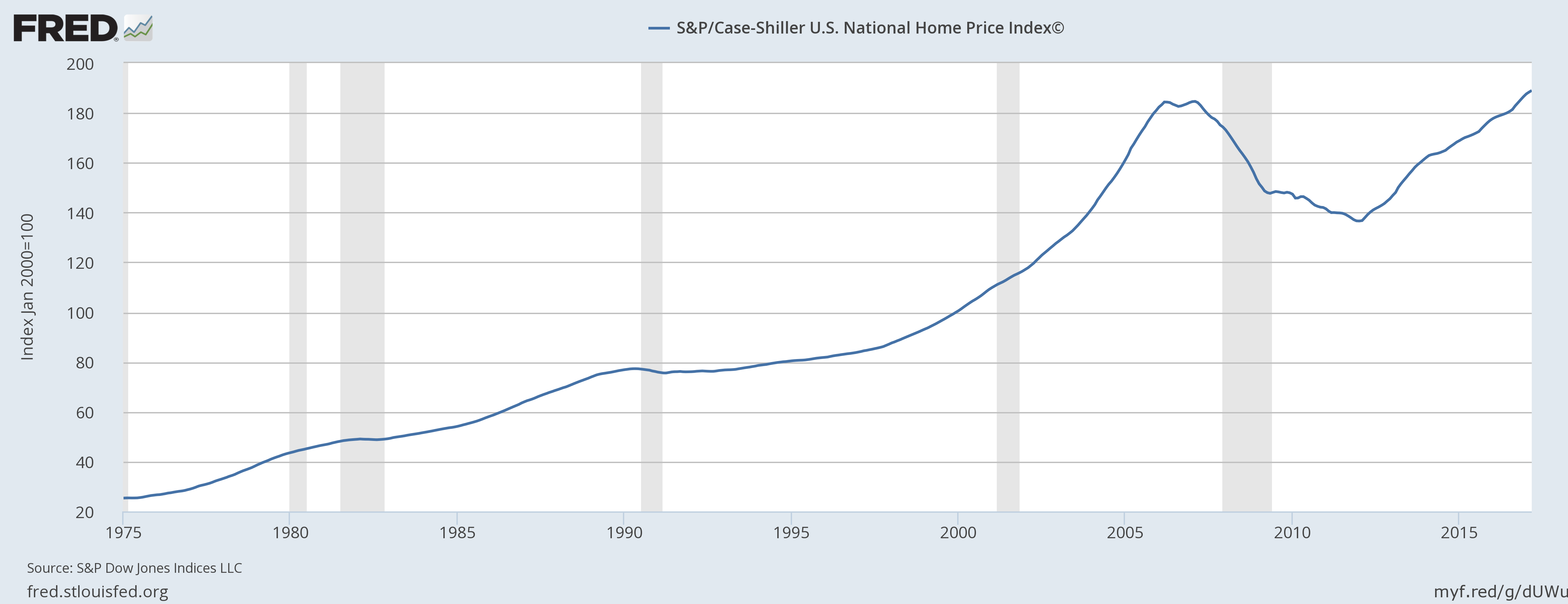

National home prices continue to move upwards. The S&P Case/Shiller National Home Price Index gained 5.5% year over year through April 2017. Current national average values are now above the 2007 peak.

In June the Federal Reserve Open Market Committee (FOMC) voted to increase the target Federal Funds rate 0.25% to 1.00-1.25%. While inflation concerns remain subdued, the FOMC saw reason enough to continue to increase rates in strengthening household spending and continued improvement in labor market conditions.

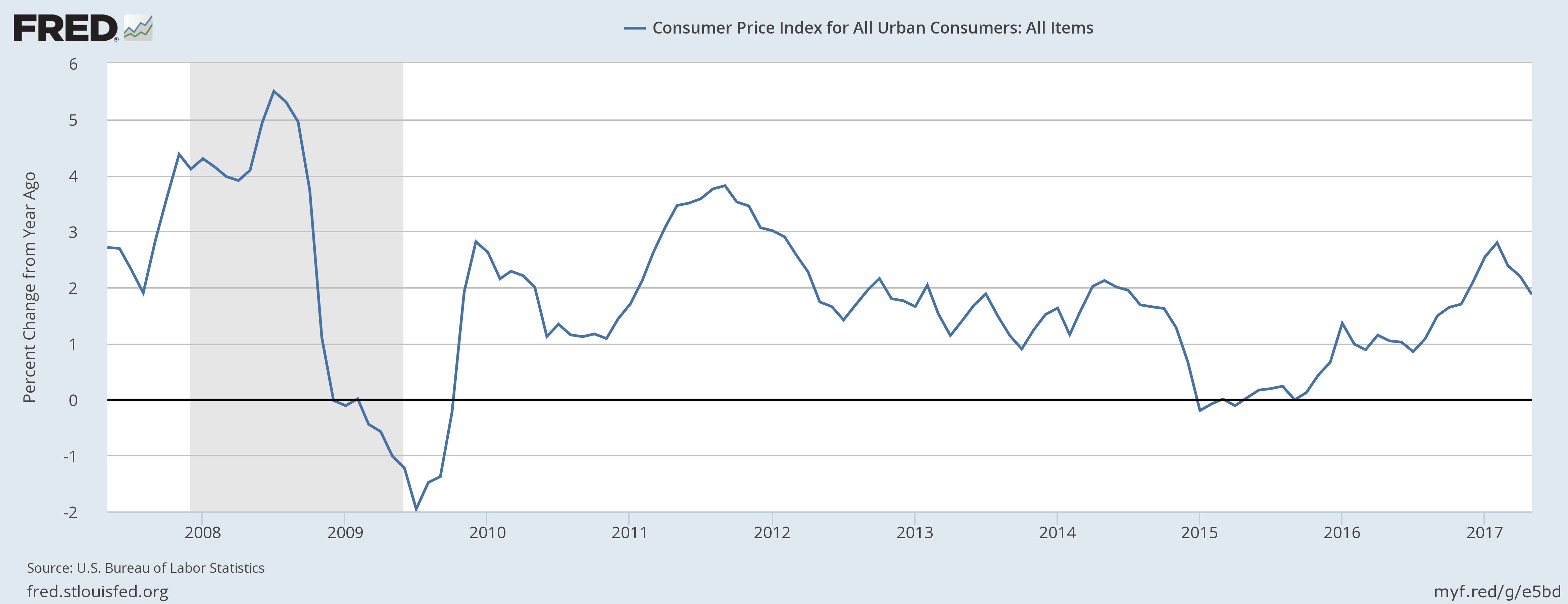

Inflation remains very low, with the seasonally adjusted Consumer Price Index coming in a just 1.87% year over year change in May, below the Fed’s 2% target for inflation.

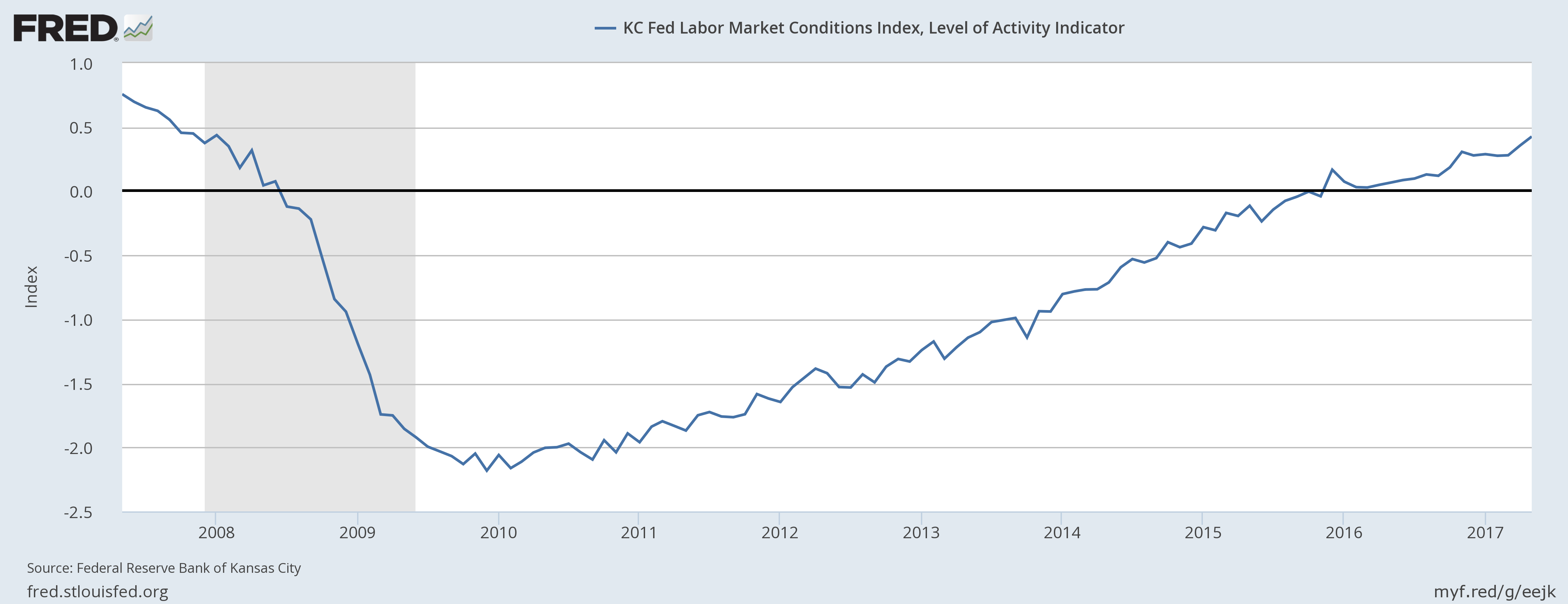

In line with the FOMC’s reasoning to raise rates, average hourly earnings of non-supervisory employees was modestly above inflation and the Fed’s 2% inflation target, with year-over-year increase through May of 2.42%. The Kansas City Fed’s Labor Market Conditions Index (LMCI) has shown a gradual increase in labor market conditions over the past several years, with a modestly positive position currently. The LMCI is an aggregation of data points on unemployment, wage, job quits, long-term unemployment, initial claims, labor force participation and several other inputs. It is a tool used to guide the Fed’s policy making.

Even with the FOMC raising short-term rates, long-term rates have not responded in kind. 30-year mortgage rates have been on the decline again, down to a national average of 3.90% through the third week of June 2017.

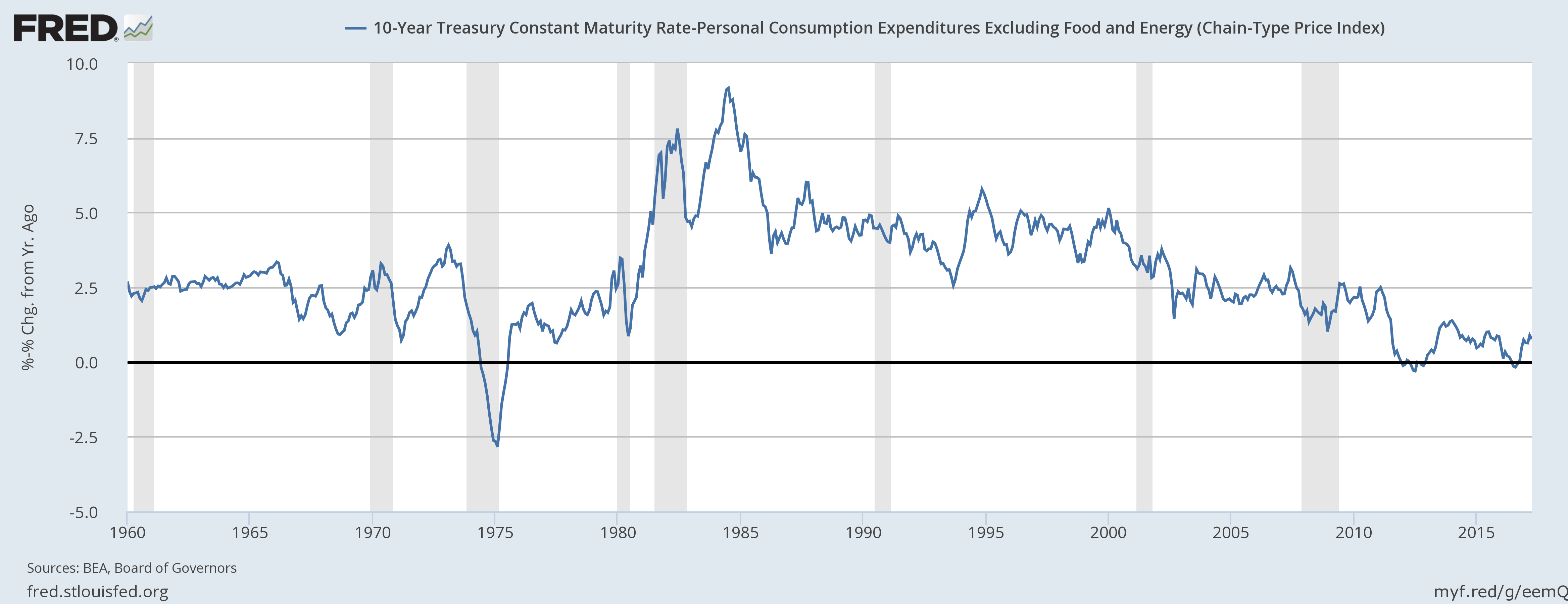

One worthwhile note on inflation: it’s low. And that is important when we are considering financial asset returns. We can bemoan l0w interest rates on savings accounts and from bond yields, but we have to remember to adjust these figures for inflation. Sure, banks paid 18% in the 80’s but inflation was extremely high as well. In fact, the period of high real interest rates from 1980 – 2000 looks as though it may be more of an outlier than lower real rates today. 2-3% real rates were the norm before inflation and rates took off around 1980.

More on this topic in a long-term context from the New York Times’ Neil Irwin a few years ago:

Very low rates have often persisted for decades upon decades, pretty much whenever inflation is quiescent, as it is now. The interest rate on a 10-year Treasury note was below 4 percent every year from 1876 to 1919, then again from 1924 to 1958. The record is even clearer in Britain, where long-term rates were under 4 percent for nearly a century straight, from 1820 until the onset of World War I.

Our perspective is distorted by anchoring, and for many investors late in their careers, the exceptionally high rates of the 1980’s coincided with early working formative years. A longer view of history makes the current environment less extreme.

Tax and Legislative Updates

Legislative priorities in Washing D.C. have shifted from the beginning of this year from health care, to tax reform, to infrastructure and now at the end of June 2017 we are back to health care reform. The Republican party controls the House, Senate and White House, and have been outspoken in their desire to replace the Affordable Care Act with their own legislation.

As of this writing, the House of Representatives has passed its version of a bill, known as the American Health Care Act (AHCA). The House version of the bill would end individual coverage mandates, employer mandates, income-based premium subsidies and the 3.8% tax on net investment income, the 0.9% additional tax for high income earners and medical device taxes. The House bill also increases the annual allowable HSA contribution limits, increases the allowable difference between premiums paid by younger vs. older consumers and brings back lifetime benefit limit caps.

Right now the Senate version is similar, as far as we know. A vote originally scheduled for Thursday June 29th was delayed so that the Senate bill could be revised after several Republican Senators voiced opposition. It is, right now, too early to say what final legislation could look like, even if the Senate version can garner the 50 votes (assuming a Vice-Presidential tiebreak) to pass a reconciled bill.

The most likely outcomes of a passed bill affecting financial planning decisions of my readers include:

- Eliminating the taxes introduced by the ACA, including the 3.8% investment income surtax;

- Revocation of individual and employer mandates (with incentives for coverage in some penalty form);

- Some change to HSA contribution rules, with likely higher limits;

- A larger gap between premiums paid by younger vs. older consumers, where older consumer would expect private-market premiums to increase;

- Changes to treatment and coverage of pre-existing conditions and lifetime limits.

Right now this remains speculation, as a vote will not occur until after the July 4th recess, and then we do not know what specifics the bill will contain, what could pass, and what could be reconciled with the House bill. For now, we have to take a wait-and-see approach, but it is possible that material tax planning opportunities may arise before year-end 2017, and that individuals purchasing private market insurance will have new rules to navigate when making selections.