Where do I begin? Unless you’ve been lucky enough to be unplugged from the world for the last 6 weeks, there is little to say. The year started off well, coming off of the spectacular returns of 2019. But as fears about COVID 19 spread and it became clear that there was a serious global pandemic on hand, markets responded quickly and severely.

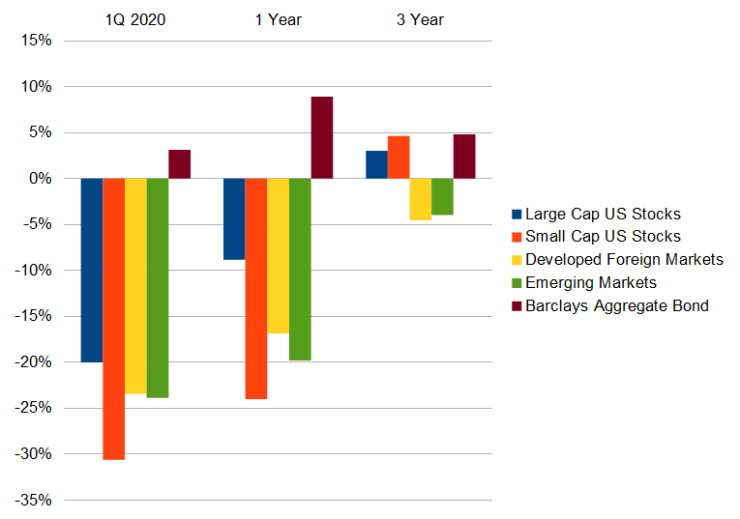

Through the end of March, Large Cap US Stocks are down a tidy -20.00% and small caps have fallen considerably more, down -30.61%. The bear market left no one out, as international stocks were also down -23.43%. Bond returns have been mixed through the rout, with the highest quality bonds like US Treasuries gaining 8.20% in a flight to quality, while corporate bonds fell slightly (-3.14%) and municipal bonds were generally flat (-0.63%).

It’s also worth noting that many asset classes that have been out of favor for some time were hit even harder by the bear market, most obviously anything related to oil and natural resources as Saudi Arabia launched a massive price war just as the global economy tipped into recession, and previously cheap small cap value stocks are, by many measures, as cheap relative to growth stocks as they have ever been.

This bear market should remind us of a few important lessons. One, bull markets don’t die of old age. There were no rules in place that the run that began in early 2009 could only go on (with a few intermittent interruptions in 2011, 2015 and 2018) for 10 years. Two, we never repeat the last crisis. The cause of this bear market wasn’t a financial system collapse or the bursting of some absurdly exuberant bull market. And lastly, three: it’s different every time. The 2000-2002 bear market was a long, slow, painfully drawn out event culminating in a total 50% drop in the S&P 500 over three years. The 2008-2009 bear was marked by a handful of steep drops that went crashing into the bottom in less than 18 months. Today’s variety was one of the steepest on record, dropping us into bear market territory in a few short weeks.

Economic Update

The economy right now is a gigantic question mark. There is no reasonable way for any of us to have an accurate estimate of the current and future impact of the pandemic on global economic activity. The information that we do have is limited and somewhat bleak. The first post-pandemic report of initial unemployment claims was a staggering 3,283,000, and increase so large over the previous period that it looks like a chart error.

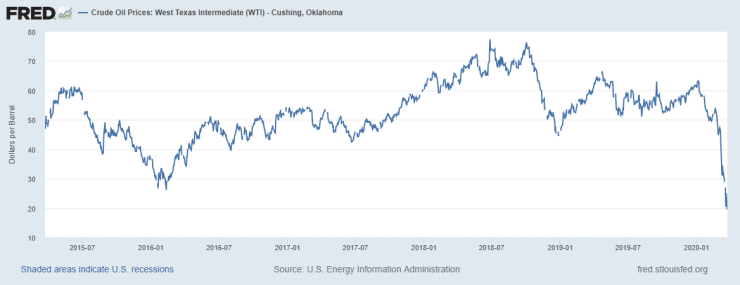

As I mentioned above, oil prices have cratered in the one-two punch of a global pandemic and a global price war. WTI Crude fell to just above $20 a barrel, the lowest price since the post-9/11 recession when global travel slowed abruptly.

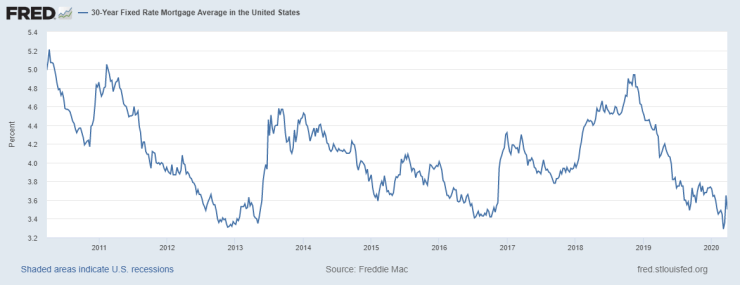

Prior to the pandemic, economic indicators looked great. Unemployment continued to fall and personal income and spending were growing on a real basis. Real estate activity was healthy and national home prices were still trending upwards. As news of the pandemic grew, interest rates fell, including mortgage rates which approached all-time lows in early March before bouncing back up in the last week or so.

As of today it is very, very difficult to see what even the current economic state looks like, let alone how and when the economy will recover from these events. Slower moving activities like real estate purchases are yet to show an impact, but we know that millions are out of work or have reduced hours and payrolls. Over the next few weeks more data will be released, providing some clarity as to the current extent of the impact of this crisis on our economy.

Tax, Legal & Legislative Updates

As a means to soften the blow of the coming recession, Congress has passed two pieces of legislation for economic relief, the most material being the CARES act, signed into law on Friday, March 27th. Some of the most key provisions are highlighted below:

- Unemployment insurance has increased to include an extra $600 per week for up to four months. For the first time, UI benefits also now cover contractors and self-employed workers. Regular UI benefits will be extended by an additional 13 weeks through 12/31/2020 and paid for by the Federal government (not states).

- A “recovery rebate” payment to individual taxpayers. This amount is $1,200 per taxpayer ($2,400 for joint filers) and $500 per child. The rebate is subject to income limitations, with a phaseout beginning at $75,000 in taxable income for single filers ($150,000 for joint filers). These calculations are based on a filer’s 2018 or 2019 income, depending on which was most recently filed.

- A new $300 “above the line” charitable deduction is available for the 2020 tax year. This means that filers who do not itemize can still take advantage of the deduction.

- Early retirement account withdrawal penalties of 10% are waived for those facing hardship due to the coronavirus. More pertinent to the readers of this message is a waiver of 2020 Required Minimum Distribution rules. No distribution will be required for IRA holders over the RMD age (now 72) for 2020. However, Qualified Charitable Distributions will still be allowed this year, providing a mechanism for taxpayers to reduce their IRA balance (and future RMDs) and receive a de facto tax break for charitable giving without itemizing. In the absence of RMDs, some taxpayers may find 2020 a good year to consider a Roth IRA conversion, which would not normally satisfy the required distribution amount, but could be an opportunity to increase your total after-tax spendable wealth.

- Small businesses (those with fewer than 500 employees) can take advantage of the “Paycheck Protection Program” which provides forgivable loans up to 2.5x an employer’s monthly payroll. These loans, guaranteed by the SBA, can be fully forgiven if the employer can demonstrate that they were used to cover payroll and necessary overhead costs such as rent and utilities. This program coupled with extended UI benefits and the recovery rebate will put billions of dollars back into the economy through individuals who receive them.

Small business owners in particular will have complex decisions to make about retaining/furloughing/laying off staff and what is best for their business and employees, be it unemployment insurance, staying on payrolls with support from the SBA forgivable loans or some combination of the two.

Again these one-year tax changes will present unique planning considerations and opportunities for many taxpayers, so please make sure that you seek good counsel in decisions relating to your taxable income for 2020.