Market Overview

Should I just re-post what I wrote for the first quarter? Markets were up strongly again this quarter. The S&P 500 was up another 8.17% in the last three months, now up 14.41% year to date. Small caps were up again as well for the quarter and are now up an astonishing 61.53% over the last twelve months. International stocks have also been strong over the last year (29.45%), and emerging markets have been positive as well (38.14%). Across the board, stock markets have gained. Bonds have bounced back some this quarter, but are still slightly down in 2021 as interest rates rose earlier this year.

| 2Q 2021 | 1 Year | 3 Year | 5 Year | |

| Large Cap US Stocks | 8.17% | 38.62% | 16.49% | 15.41% |

| Small Cap US Stocks | 4.29% | 61.53% | 13.09% | 16.02% |

| International Equity | 4.37% | 29.45% | 5.58% | 7.46% |

| EM Equity | 4.42% | 38.14% | 8.73% | 10.51% |

| Aggregate Bonds | 1.83% | -0.33% | 5.34% | 3.03% |

Index performance is provided as a benchmark. It is not illustrative of any particular investment. An investment cannot be made in an index. Past performance is not an indication of future of results. S&P 500, Russell 2000 Index, MSCI EAFE Index, MSCI EM Index, BBgBarc US Agg Bond Index. Returns as of 6/30/2021.

I get the impression today that the general feeling is one of waiting for the other shoe to drop. Everyone I talk to is looking over their shoulder, expecting the stock markets to come crashing down any second. So for something like the 10,000th time, I’ll say: I have no idea what happens next. Are the markets “too high”? What does that even mean? Yes, sometimes some stocks get expensive relative to historical measures. Sometimes they get cheap too. If you think you can use those measures as a timing tool, Godspeed. It’s never been done successfully before.

Once again, this is how markets work. We don’t get 9-10% equity returns year after year like a nice tidy CD or bank account. We get uncertainty, doubt, fear, greed, FOMO and the whole bag of human emotions interacting with stock prices in the short-term. Market returns aren’t neat or tidy, they aren’t predictable and don’t come wrapped up with bows on top. They come when they do, not when you want them to or when you think they should.

So we’ll take these returns when they come, knowing the downturn is somewhere in the future, knowing it will be temporary and that our financial plans are robust enough to survive it. And we’ll stick to those plans and move on with our lives.

Economic Update

For all the talk of overheated stock markets, the US economy is doing quite well, thank you very much. Nearly all measures are showing positive signs of economic growth, from labor markets, real estate to inflation and consumer confidence.

Personal income in the United States is strong, with a combination of falling unemployment, rising wages and stimulus payments. While stimulus payments make this chart quite ragged, the general trend in incomes is clearly higher.

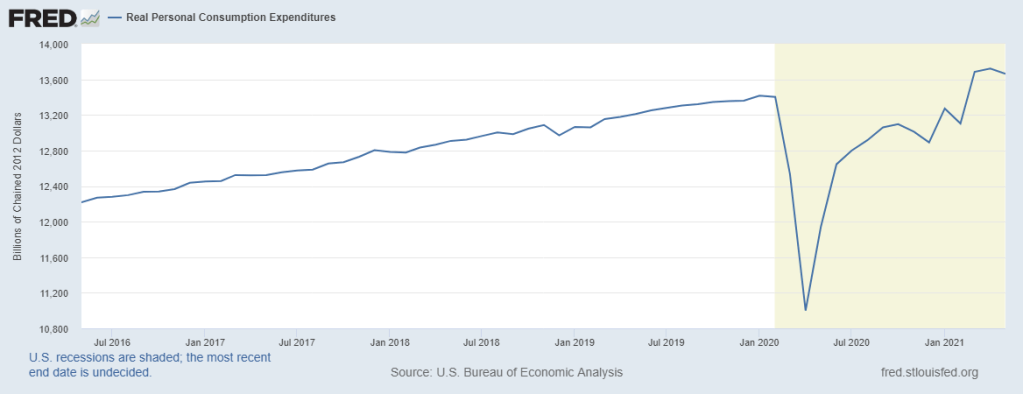

Personal spending has kept track with rising incomes as the American consumer finally feels post-shutdown/lockdown relief and lets free much pent-up demand from their wallet.

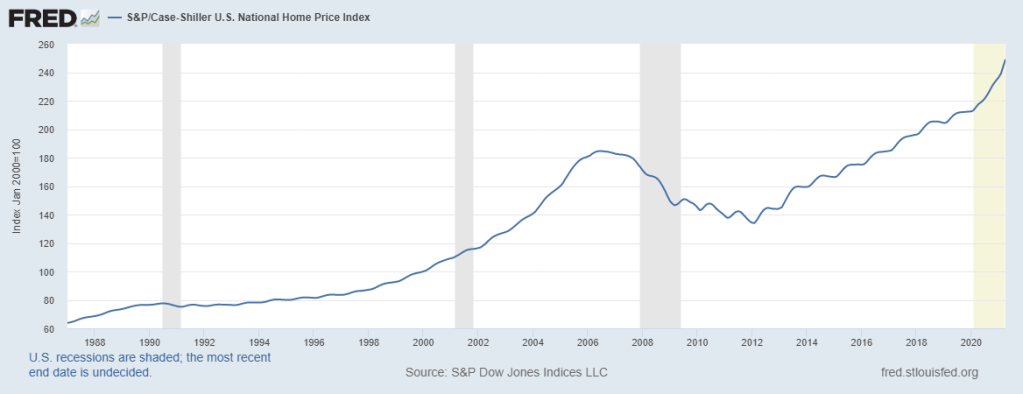

One of the biggest stories in the current economy is residential real estate. Home prices continue to soar nationwide as inventories are strained and mortgage rates hover just above all-time lows from earlier this year.

Inventories crashed during the pandemic and have made no effort at recovery. Active listings remain near historic lows, driving prices higher.

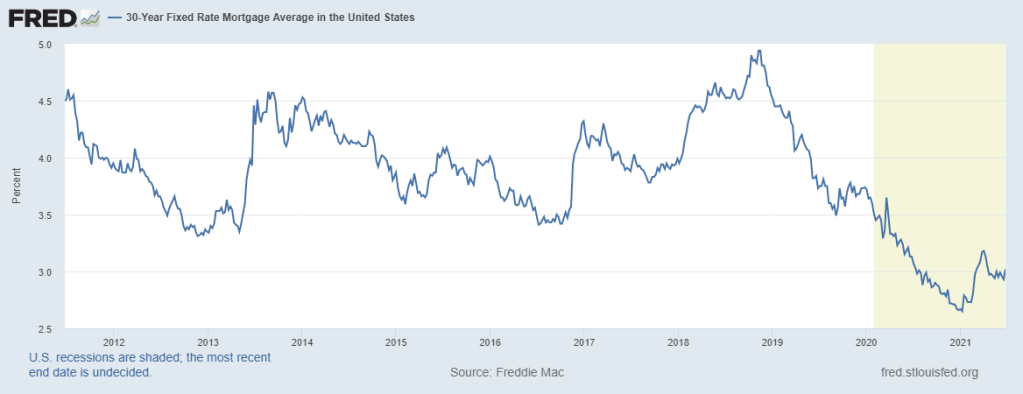

Mortgage rates bottomed in early 2021 and have bounced somewhat but remain low by any historical measure.

The Federal Reserve has left the Fed Funds rate unchanged, citing expectations of transitory inflation and still elevated unemployment levels. Initial claims for unemployment continue to fall as the labor market tightens. The unemployment rate has fallen to 5.8% in May 2021.

Wage growth has been very steady in the 3-4% range for the last 12 months. Monthly growth has surprised to the upside, at 0.5% in May alone for all private market nonfarm payrolls.

Tax & Policy Updates

There has been a fair amount of noise but little to no activity out of Washington from a tax and policy standpoint this quarter. The stimulus package from earlier this year is in effect, including monthly refundable payments for the new child tax credit (beginning July 2021).

President Biden has proposed a large tax bill, which is of course popular on the left in DC and facing resistance from the right. It’s very important to remember that this is a proposal only and very rarely do such presidential wishes come fully true, even when the president’s party has control in congress. The proposal would increase the top tax rates back to 39.6%, increase taxes on capital gains for taxpayers with income over $1,000,000, tax capital gains at death for gains over $2,000,000 for married couples and increase the corporate tax rate from 21% to 28%. As of today, this is all speculative.

Most of the energy in Washington right now is focused on an infrastructure spending bill, already caught in the intra-party quagmire between moderate and liberal democrats. While there is some bipartisan consensus around a $1.2T policy proposal, we really have no idea what a final bill could look like until there is a final bill to look at.

For personal investors, the best course of action right now is to not panic about these proposals, not make rash changes to well-laid plans and carefully consider any actions to move away from your previous plans. While policy is important from a planning standpoint, tax policy doesn’t move markets the way so many people fear as the global economy is simply too broad and complex to be pushed around by a single issue.