Market Overview

2014 proved to be a diverse year for market returns. Once again US stocks outpaced their global counterparts by a very healthy margin as the S&P 500 gained 13.69% and the MSCI EAFE lost -4.90%. Small cap US stocks, after lagging most of the year, had a strong fourth quarter with gains of 9.73% to finish up 4.89% for 2014. US Real Estate rebounded in 2014 after a weak 2013, gaining 28.68% for the year. High quality intermediate term bonds had a very solid year as interest rates again surprised most forecasts and ended the year lower, with the 10-year US Treasury down to 2.17% on December 31.

2014 was not an easy year to be a well diversified investor. Short term bonds were lackluster. Value and small cap US stocks lost out to the S&P 500. International stocks, including small caps and emerging markets, posted negative returns while the US market went on for a great year. It has been an easy year to question your investment strategy. Should you still be globally diversified? Should you have less in international? Less in small caps or value stocks? It is crucial to remember that markets go in cycles – what is in favor for a period will be out of favor soon enough. For some perspective, let’s take a look at global valuations – how cheap or expensive are certain markets relative to their earnings?

You can see that the US is the most expensive (has the highest Cyclically-Adjusted Price/Earnings ratio) of the major developed markets, nearly twice that of Europe and emerging markets. I’m not trying to make a market timing call here – I am just pointing out that markets and asset classes that have underperformed are now cheaper (sometimes by half) than the US market which has outperformed. This is common sense, but we occasionally need reminders. These things are cyclical:

Don’t forget this fact, and don’t throw in the towel because you think your strategy is “broken.”

Economic Update

The full year 2014 continued to bear out the slow-but-improving economic environment we’ve seen for the past few years. GDP growth throughout the year was reasonably strong. The most recent revision to third quarter GDP growth was an impressive 5.0%.

The employment picture is improving as unemployment dropped below 6% for the first time since 2008, and wage growth has been muted but positive.

Inflation has been a non-event for years, and expectations for the coming several years are low.

Energy prices, a significant contributing factor to overall prices, have taken a sharp drop in the second half of this year. This has led to a further drop in the inflation rate in the past six months. The fall in energy prices has spurred massive speculation about the causes of price changes, impact on corporate investment and consumer spending. As I’ve commented previously, lower energy prices may have a negative short-term impact on the energy sector of the markets but a possible offsetting positive impact on consumer spending and related sectors. Ultimately, no one can predict the outcome of such a complex system as the global economy.

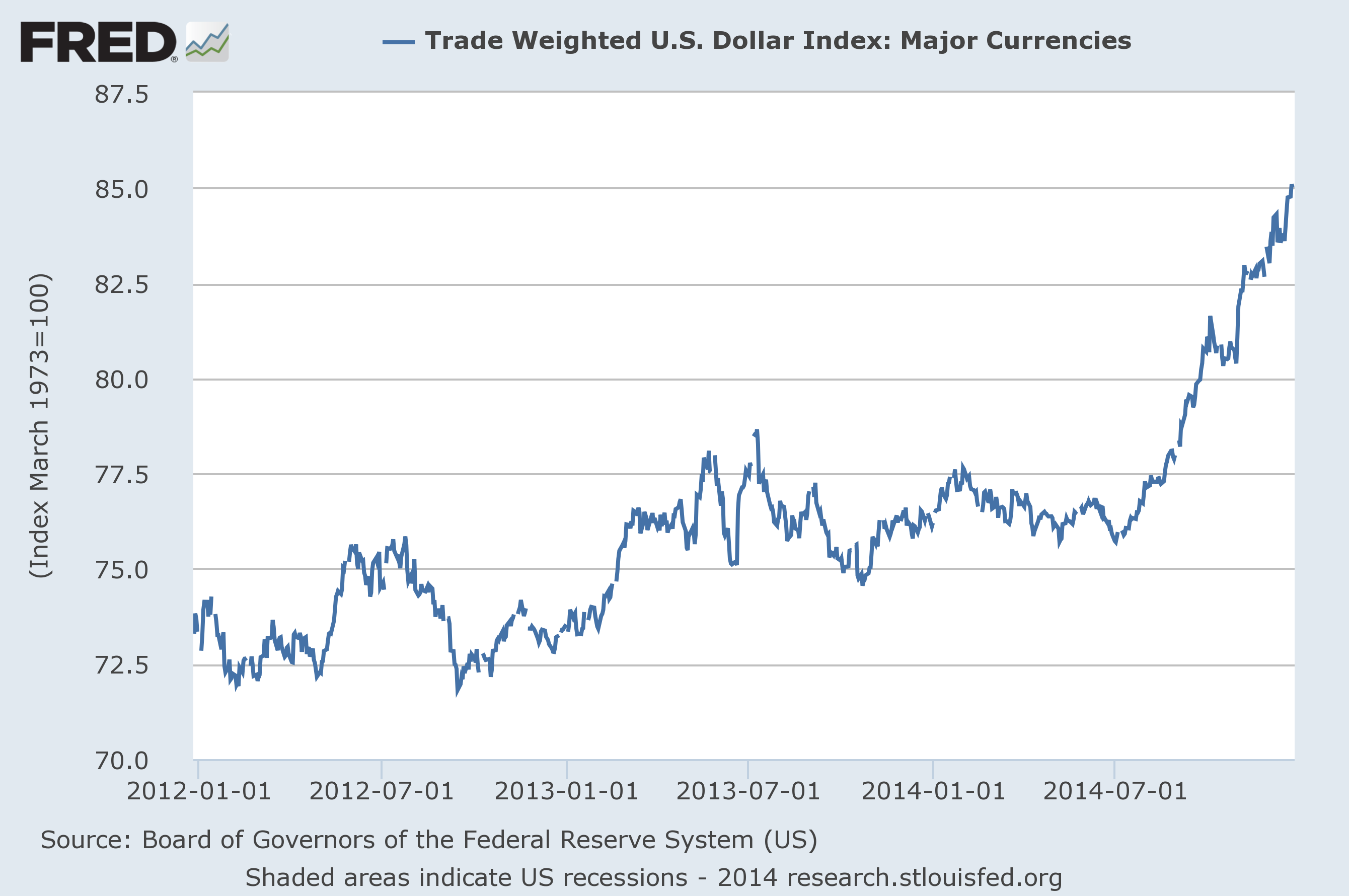

The last major economic news of 2014 was a tremendous rally in the US Dollar:

Against a trade-weighted basket of major foreign currencies, the dollar has gained roughly 11.5% through the last full week of December. Market expectations of additional monetary stimulus in the Euro zone and Japan coupled with the end of Quantitative Easing in the US have boosted the relative value of the dollar. This had immediate impact as falling international currency prices dragged on returns realized by US investors who own foreign stocks. The economic impact is more complex – a strong dollar is better for commodity consumers (you putting gas in your car and heating your home), as well as those consuming imported goods, including “imported” (outsourced) labor. It can make life harder for commodity producers and net exporters. It may make your European vacation and that bottle of Spanish wine cheaper, but it may be more expensive for GM to sell cars to India and China. As with practically everything in economics, there are winners and losers.

Taxes & Politics

Below is a quick summary of things that changed in 2014 and are changing for 2015:

– President Obama’s new retirement savings initiative, the myRA, has begun. The myRA is essentially a Roth IRA ($5,500 contribution limit, no tax deduction but tax-free growth if funds are used for retirement). The only investment option in the myRA is a conservative government bond fund very similar to the “G” fund in the federal Thrift Savings Plan, and the myRA has a maximum account balance of $15,000. In essence, the plan is designed as a beginning savings strategy for those who do not have a workplace retirement plan and have not taken the time to set up an IRA personally, but woudl like to have payroll deductions made to a retirement account.

– In 2015 we will see increases to the maximum contribution limits for 401(k)s and similar vehicles, defined benefit plans and SIMPLE IRAs. 401(k) deferral limits are rising from $17,500 to $18,000. 401(k) plan catch-up contributions will be increased from $5,500 to $6,000 next year. SIMPLE-IRA limits will grow from $12,000 to $12,500. There will also be an adjustment in the Social Security wage base, increasing the amount of earnings subject to FICA taxes from $117,000 to $118,500. Social Security recipients will also see a benefit increase of 1.7%.

– The cliff for itemized deduction of medical expenses has risen from 7.5% to 10% of a taxpayer’s adjusted gross income as a result of the Affordable Care Act. This will reduce the amount of medical expenses that can be deducted, all else equal.

-Beginning January 2015, investors will only be allowed to make one rollover of an IRA per calendar year. An rollover is a withdrawal from one IRA that is held for less than 60 days and then deposited into another IRA. This law does not affect trustee-to-trustee transfers (such as moving a brokerage account from Fidelity to Charles Schwab) or retirement plan rollovers, such as from a 401(k).

– After the court ruling in Clark v. Rameker, inherited IRAs will see decreased creditor protection in 2015 and beyond. The US Supreme court ruled that inherited IRAs are not retirement funds and as such are not given the same sheltering protection as IRAs, Roth IRAs 401(k) plans and pensions.This lack of creditor protection may lead some to revisit leaving large IRAs directly to beneficiaries and consider using spendthrift trusts if creditor protection is a major concern. Of course, these decisions can have significant tax consequences, and should be carefully evaluated by your legal, tax and financial professionals.

As always, I won’t speculate as to what 2015 may bring. Investors will be best served by not trying to guess what happens next and instead investing sensibly by using an investment policy statement, keeping their emotions at bay and focusing on the things we can control.