Market Overview

In the first quarter of 2015 we finally departed from the performance leadership of large cap US stocks. The S&P 500 squeaked out a positive return of 0.95% over the past three months which was dwarfed by strong performance in small cap US stocks and international developed markets, up 4.32% and 4.88%, respectively. Once again, despite ongoing fears of rising interest rates, bonds performed admirably, up 1.61% in the first quarter and 5.72% over the past year. Emerging markets managed a gain for the quarter, up 1.91%, but still have been down -2.02% over the trailing twelve months.

Not shown in the chart above is US real estate, up 4.58% for the quarter and an astonishing 22.94% over twelve months.

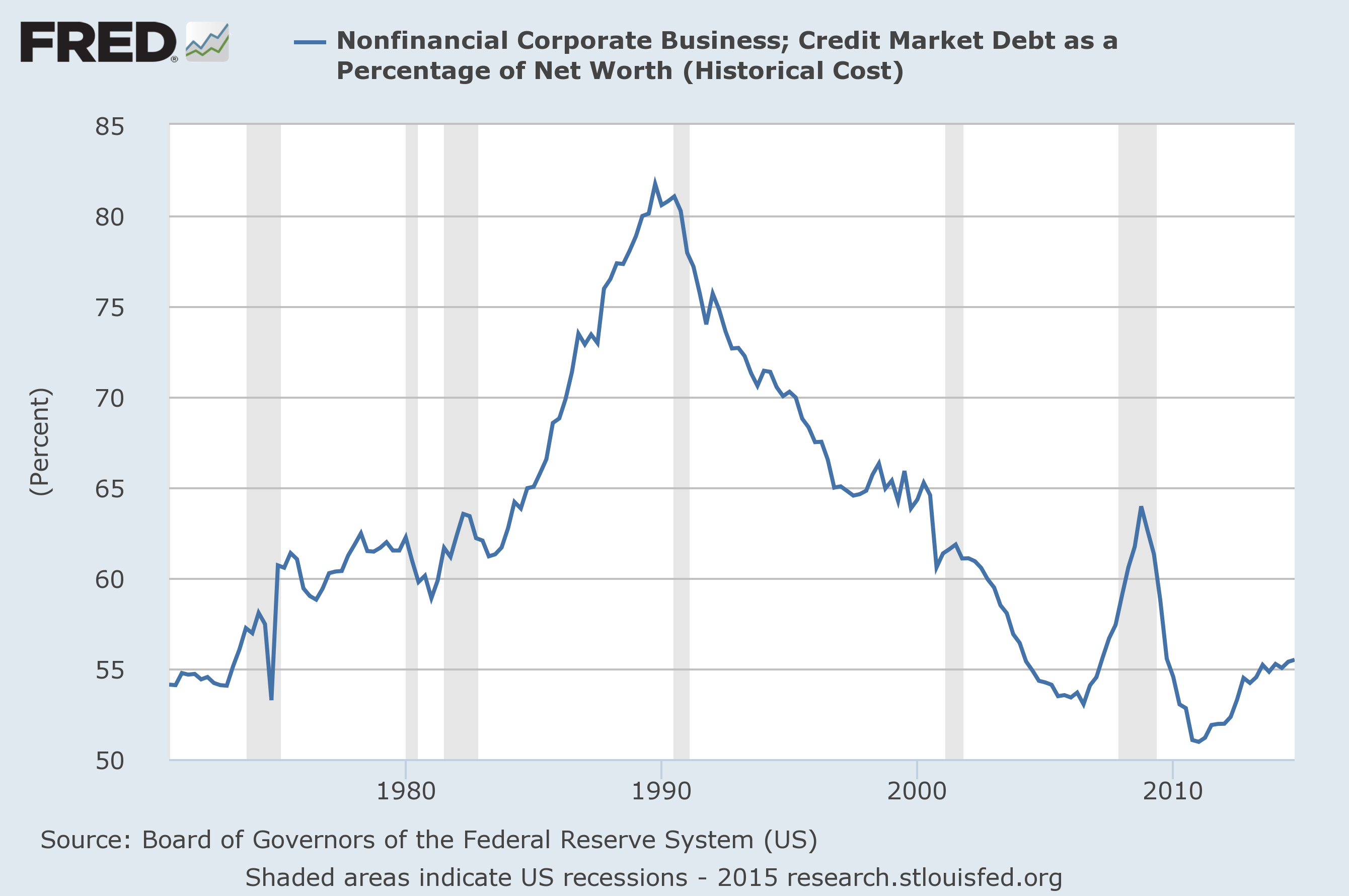

Despite regularly increasing dividend payments and share repurchases by public US companies, corporate balance sheets remain in remarkably good shape. Cash as a percentage of current assets has been in a steady uptrend since the bear market of 2008-2009, and corporate debt as a percentage of balance sheet values remains at or below historical averages.

S&P 500 Companies have seen reasonably steady growth in quarterly earnings after coming out of the financial crisis, with the occasional temporary drop as to be expected.

Economic Update

There are two main stories about the economy in the first quarter: the huge gain in the US Dollar against foreign currencies and a strengthening labor market. The trend of the upward moving US Dollar that began in late 2014 continued into the early part of 2015, up another 7% through late March.

For US owners of international investments, this gain has been a drag on returns. For example, currency changes wiped out nearly half of year-to-date 2015 returns for the benchmark MSCI EAFE index, which was up over 10% before the currency adjustment back to US Dollars. The same affect was in place in 2014, with the MSCI EAFE actually up 6.4% in local currencies, but down -4.5% after adjusting to the US Dollar.

In the 2012 Credit Suisse Global Investment Returns book there is an excellent study demonstrating that the impact of currency exchange rates for long term investors is negligible and hedges should be avoided. Over time, currency exchange rates swing back and forth between a stronger and weaker US Dollar (as you can see in the chart above). Like most investment decisions, investors currently exposed to foreign currencies through international stocks or bonds in their portfolios would be wise not to panic about the current move in exchange rates and instead stick to their long-term plans.

From an economic perspective there are endless debates about whether a stronger US Dollar is good or bad for the economy. It breaks into one simple piece: a strong currency is good for importers (buying goods and services internationally) and bad for exporters (selling goods and services internationally). Goods produced in the US and sold internationally become more expensive, but those imported (including “imported” labor via offshoring) become cheaper. It will be a boost to US residents traveling abroad, and dampen the spending ability of international travelers to the US.

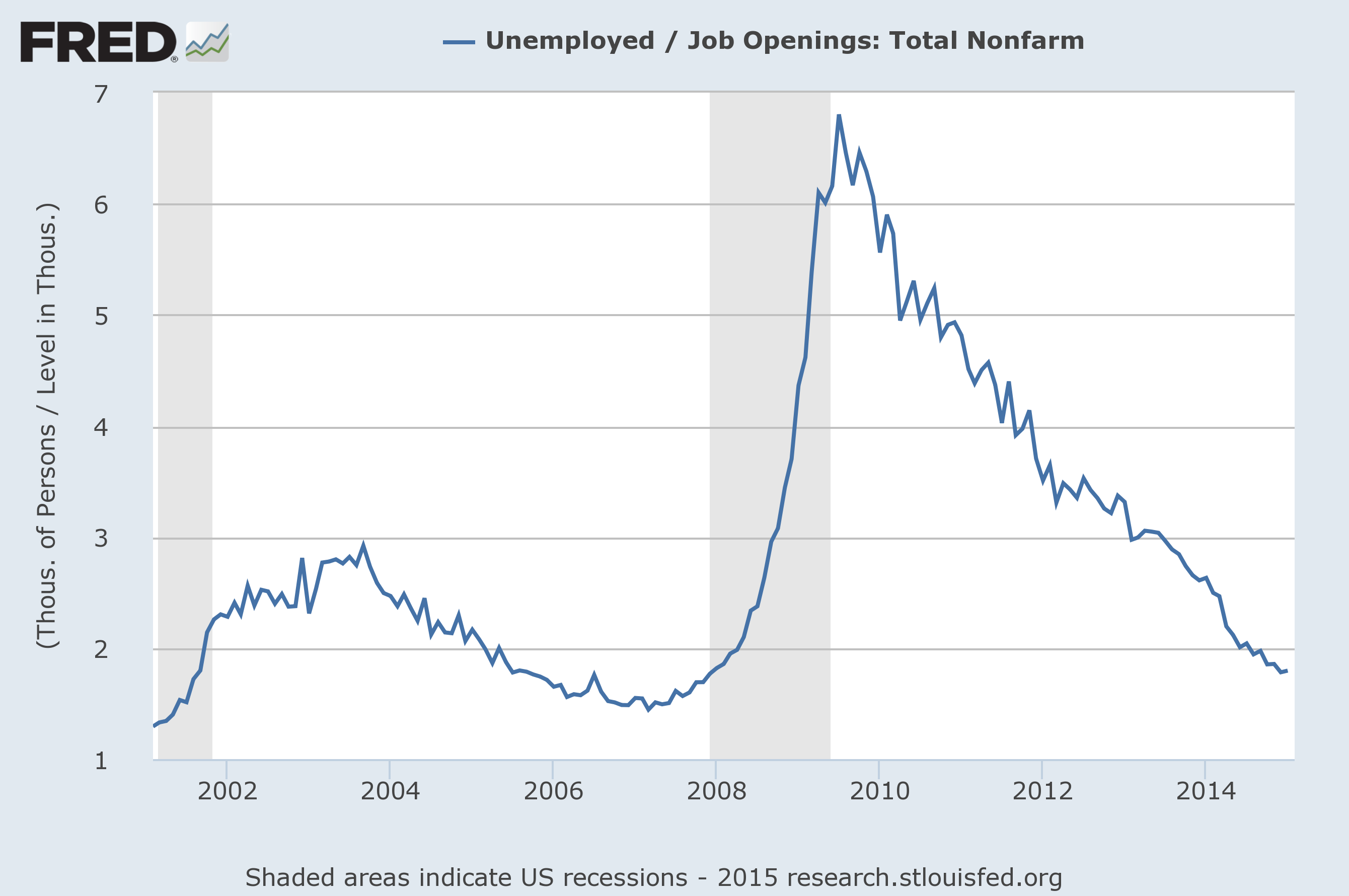

The second major story in the economy this year has been a shift in the balance between the labor force and employers. As we might expect this far into a growth cycle, unemployment is back to normal levels and the pool of available candidates for job openings is shrinking. The count of individuals making an initial unemployment claim has fallen dramatically in the past few years:

And below, the ratio of unemployed individuals to available job openings is back to pre-recession levels.

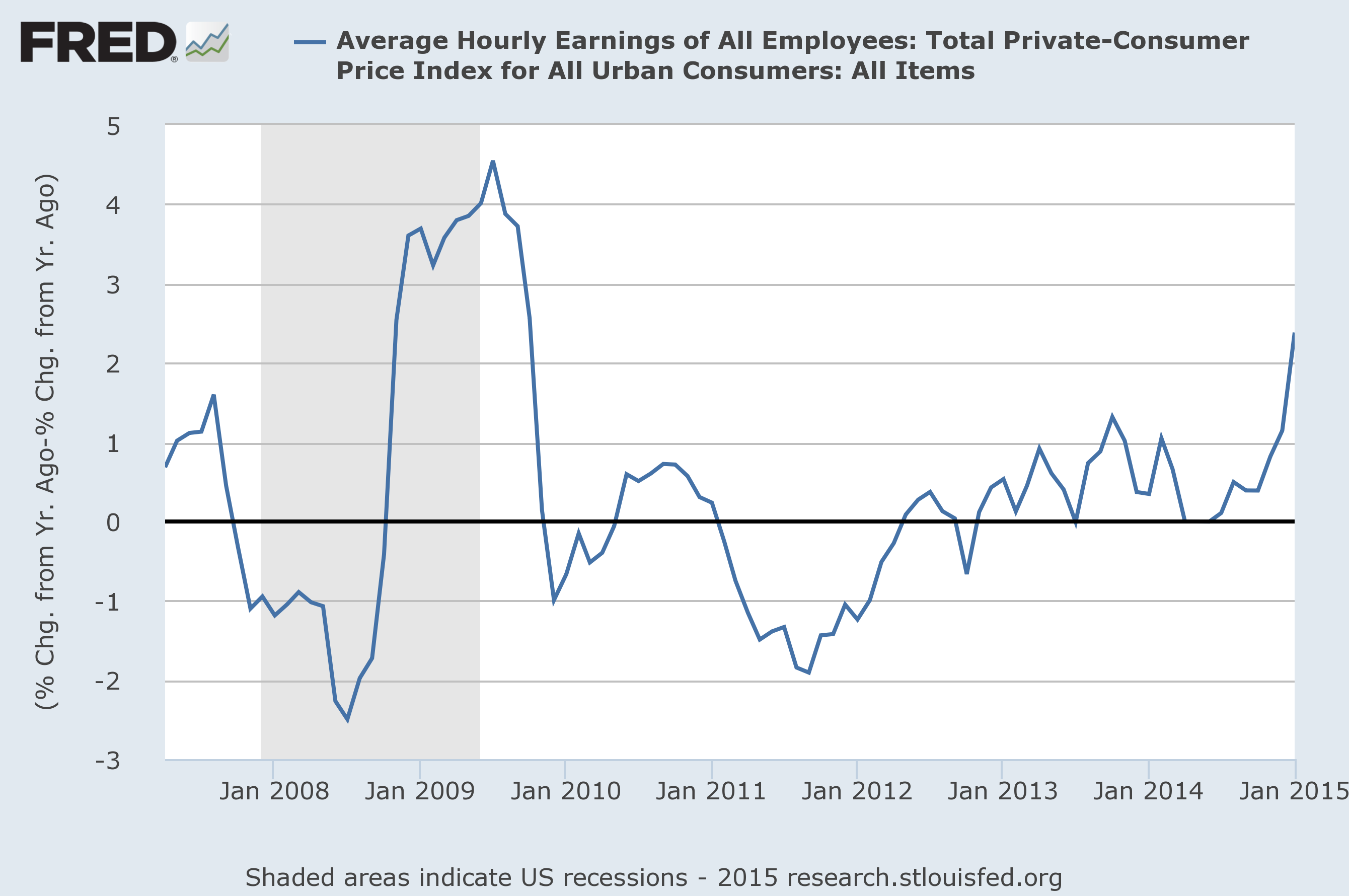

With fewer and fewer available candidates for hire, corporations are finding the need to raise wages to stay competitive. News stories are rolling out: McDonald’s increases wages for corporate hourly employees. Wal-Mart also raises wages above the minimum wage. Last year Gap and Ikea did the same. While these wage increases will take time to ripple through the economy and show up in the data, it’s fairly safe to say a trend is in place in keeping with this stage of an economic cycle.

In part thanks to very low inflation, employees have seen real (inflation-adjusted) wages grow slightly over the past few years. In addition, falling oil prices have amounted to the equivalent of a large tax break to the average American consumer. The average American household spends 6-8% of their total income on gasoline.

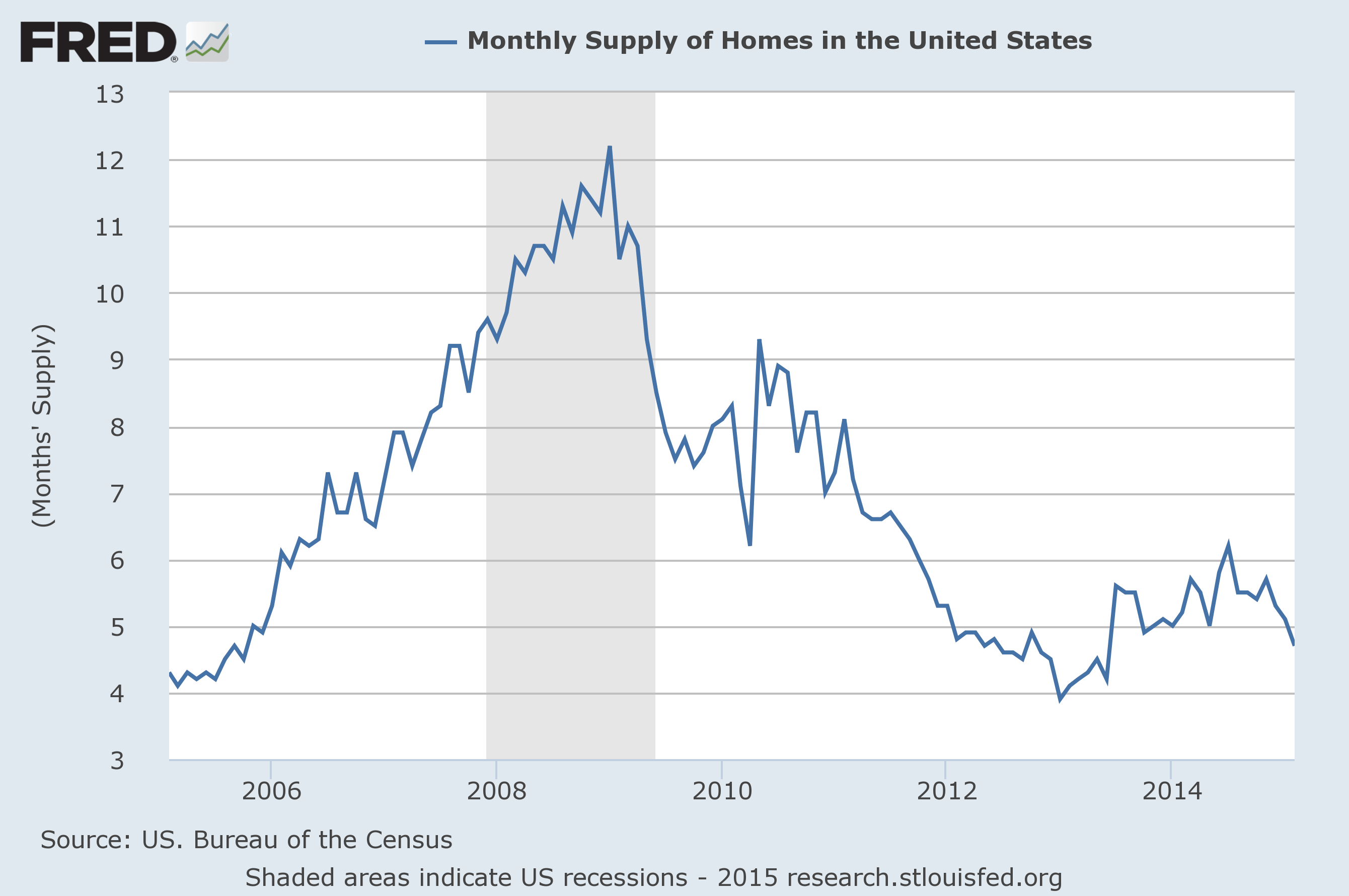

More broadly, the housing market in the United States is tightening. Home inventories have been falling to historically low levels. Years of small amounts of new construction have caught up with the economy and permits for new home construction are on the rise.

While still above historical norms, mortgage delinquency rates continue to fall, more evidence that the average US household continues to see improvements in financial status.

Tax

It’s tax time, and the window for taking action to have an impact on your 2014 income taxes is closing rapidly. Individuals considering contributions to retirement accounts for the 2014 tax year, including IRA, Roth IRA or Individual 401(k) contributions need to move quickly to meet the 4/15 deadline. Of course, the best tax planning is done in advance and it is always the right time to be thinking about your current year tax situation. Individuals and businesses have much greater control over their tax situation if planning is done earlier in the year.