Well. Here we are, folks. You just went through one of the most dramatic declines in US stocks in a single quarter in decades. How’d you do? Did your life change materially? Did you spend time on a daily basis staring at a screen, slowly descending into a mild state of panic?

From 10/1/2018 – 12/31/2018 the S&P 500 fell a total of -13.58%. The top-to-bottom decline (based on daily closes) barely escaped the technical definition of a bear market decline of 20%. Yes, it happened quickly. No, you didn’t see it coming. No, you don’t know what happens next week/next month/next quarter. Are we done? I have no idea. No, you don’t know why it happened now or why it happened like this or why we had some days with 3% swings throughout the day. Neither does your brother-in-law, the President of the United States, Rand Paul or Jerome Powell. You can say it is because of the trade war or the Federal government shutdown but the reality is those are stories we made up after the fact.

This quarter should be a gut-check, a long-overdue reminder that this is what markets do. Most of the time (say, from 2009-9/30/2018), they go up. Sometimes, they go down. Sometimes they go down a lot, sometimes they go down quickly. Sometimes those declines last, sometimes they are short lived. Sometimes they precede a recession, sometimes they don’t. Don’t ask me which one we’re in now, and don’t fool yourself that you already know. You don’t know.

What you can do today is take a breath. Use this as a chance to double check yourself as an investor. What does your investment policy say to do in these environments? Maybe rebalance? Take some tax losses? Systematically invest new cash according to a pre-set allocation? I’m guessing your investment policy doesn’t say things like “Speculate wildly on Twitter about today’s close,” or “Sit nervously in cash until your gut feels better about politics” or “Listen to the guys at the gym and do what they are doing too.”

Next, double-check your long term plan. Did a <20% stock decline ruin your long-term prospects? (Spoiler alert: it didn’t.) If you had any reasonable long-term plan, this is part of it. Only a complete fool would build a long-term plan that involved investing in stocks and didn’t bake in a bear market not just this one time, but on a pretty regular basis. Say at least once every 3-5 years on average. While this one came fast, let’s be perfectly clear: a <20% decline in stocks is A PERFECTLY NORMAL, AVERAGE, REGULAR OCCURRENCE IN STOCK MARKETS. Okay? It’s nothing else except something that happens with frequency. Unpredictable, yes. Unexpected, no. So now you know your financial world has, in fact, not crumbled.

Lastly, take your pulse. Are you losing sleep? Pulling out your hair? Convinced the end is nigh? Are you running a constant ledger of the value of your portfolio compared to the highest it was ever valued, and judging your personal self-worth as a human being accordingly? While I sincerely hope none of us have adopted the last practice, this is a good chance to really find out how much downside you can emotionally handle in your portfolio. Everybody is a risk taker when stocks are on a never-ending ascent. Investment risk means something entirely different when you’ve seen the markets eat the last several weeks/months/years of your retirement account savings contributions. If watching the markets fall 20% is ruining your mental health, maybe your investment strategy is a poor fit for your personality and psychology.

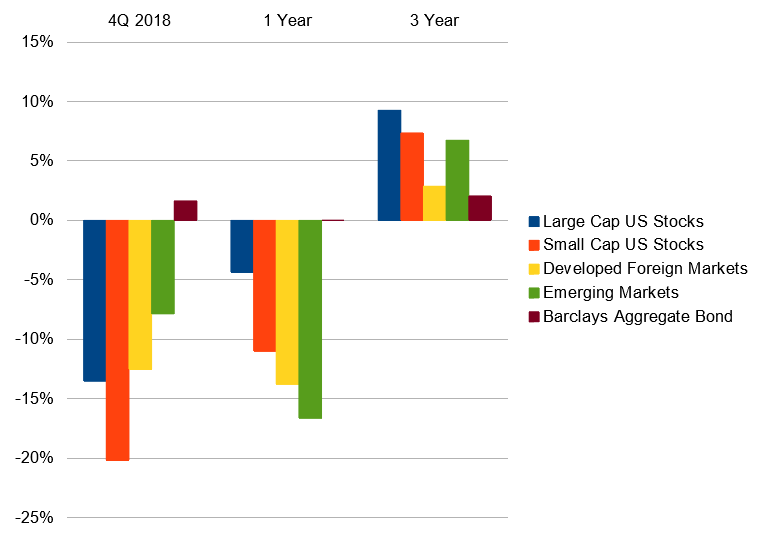

Here’s where we really stand through 12/31/2018:

Most global stocks were down for the year, small (-11.01) to large, US (-4.38%) to International (-13.79%). Things that held up reasonably well earlier this year fell more heavily this quarter, led by small and large US stocks. Bonds held their own, with municipals posting modest gains for the year (1.28%) and broad US taxable bonds almost perfectly flat (0.01%).

Economic Updates

Despite our collective madness around stock prices in the last few months, the global economy has yet to fall off a precipitous cliff. While a few areas (including real estate) have shown a little softening, the broad data still looks very solid.

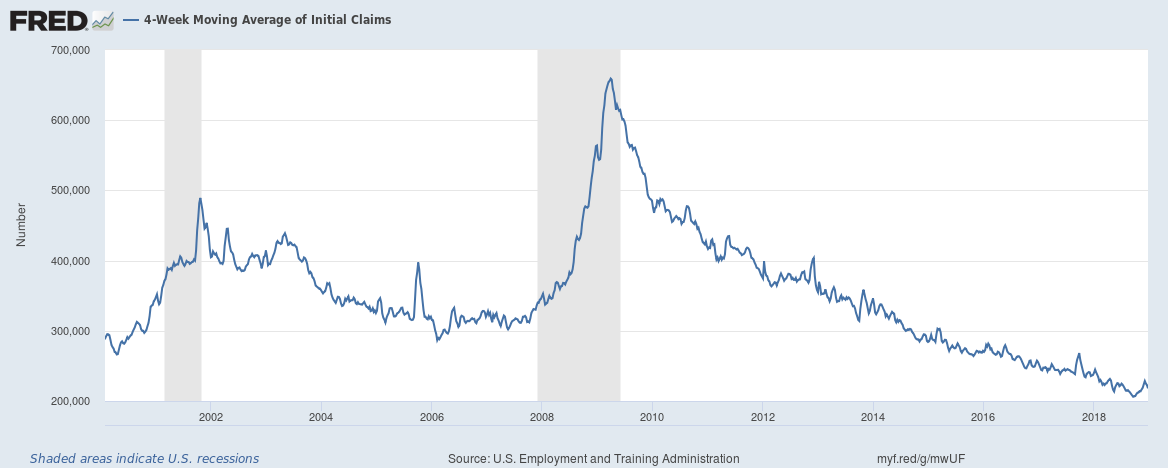

US workers and consumers have a tailwind. Unemployment is low, job openings are abundant, initial unemployment claims remain very low.

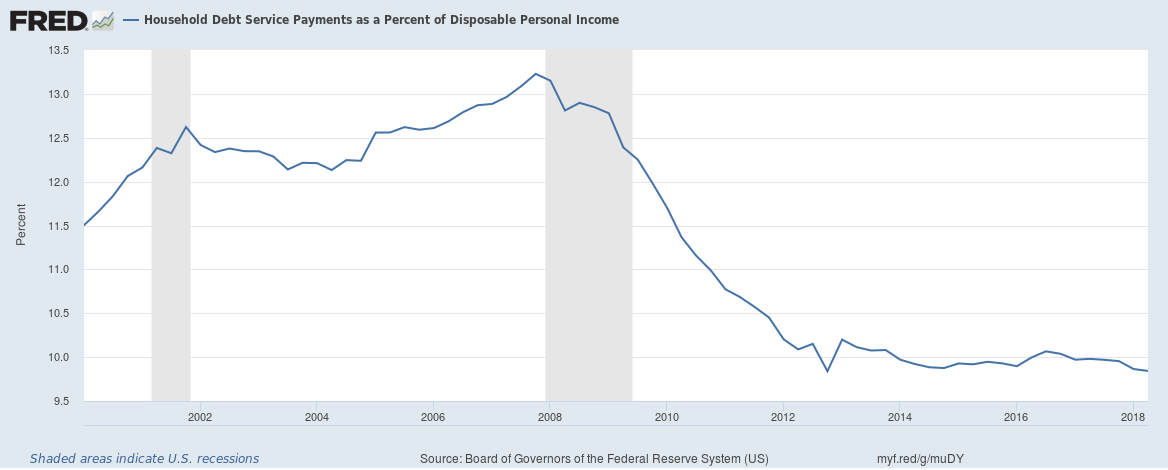

Consumer balance sheets are healthy, mortgage delinquencies remain low and household debt service is affordable.

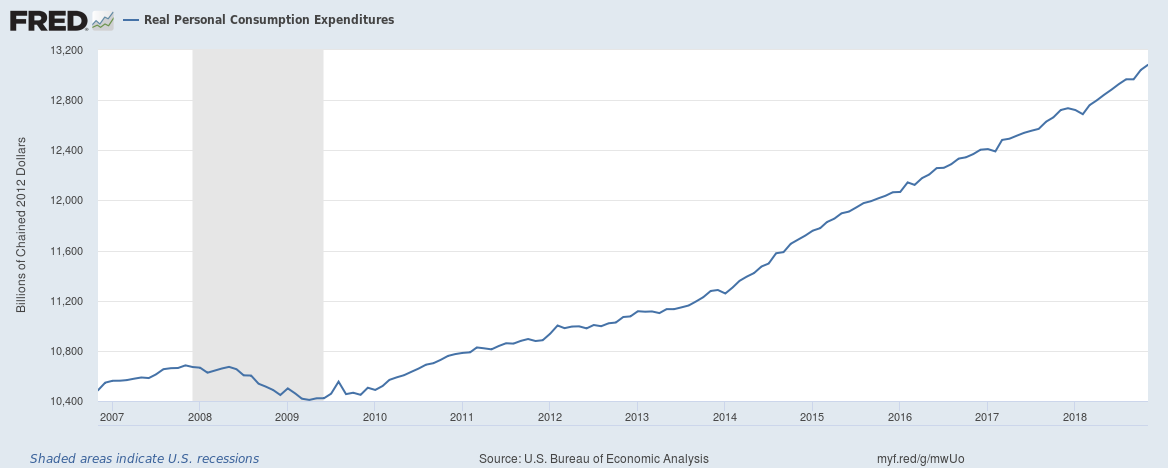

Consumer spending (that is, Real Personal Consumption Expenditures) gained 0.4% in November, just above the growth in real personal income (0.2%). You can see this number has steadily climbed after the downturn in the 2008 recession.

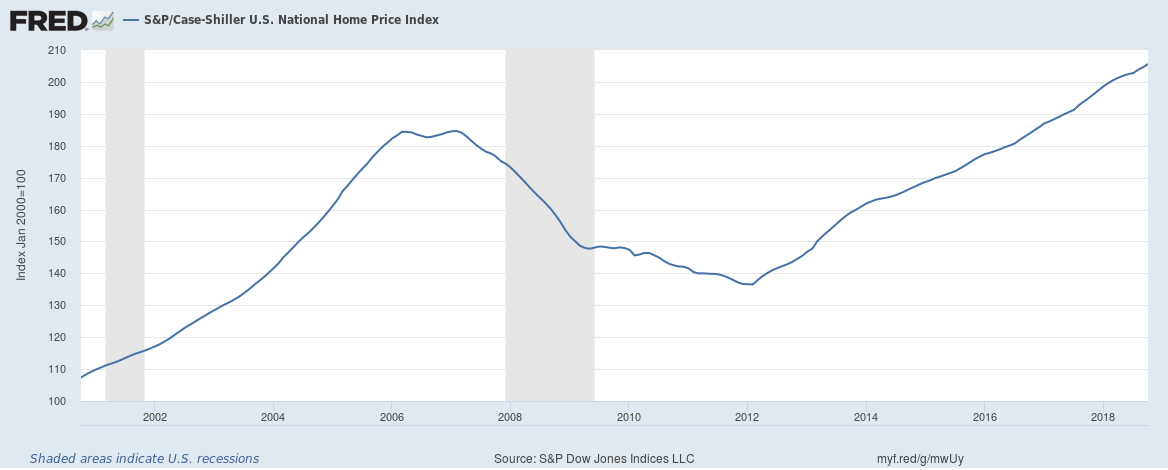

If anything in the US appears to show signs of softening, it is the residential real estate marketplace. After several years of catching up and a few areas with rapidly rising prices, the rate of price changes has slowed. Rising interest rates may also be contributing to weakening demand as mortgage payments increase proportionately. In October 2018 the Case Shiller national home price index gained 5.5% over the previous year, a more moderate figure than the last few years.

New home construction has steadily climbed off the post-recession bottom over several years but has recently started to level out.

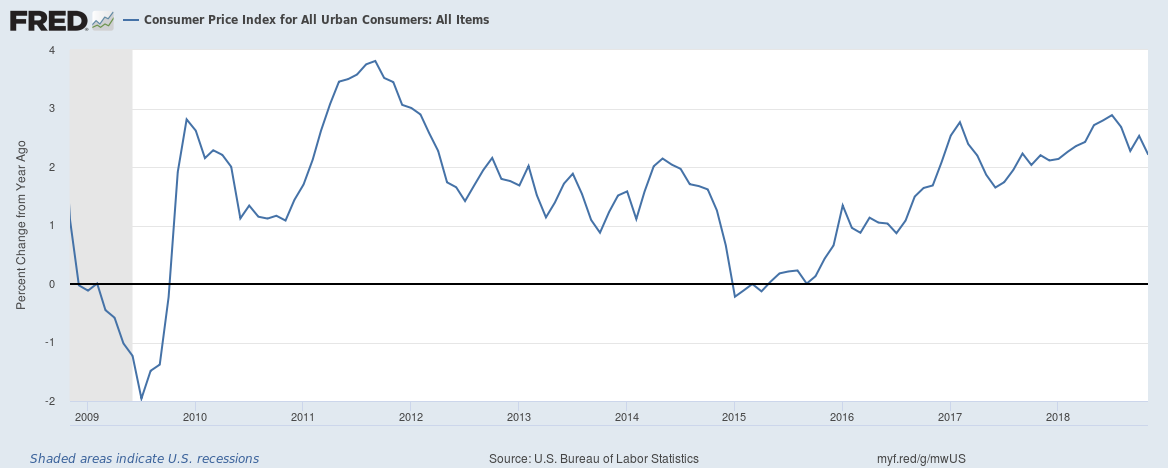

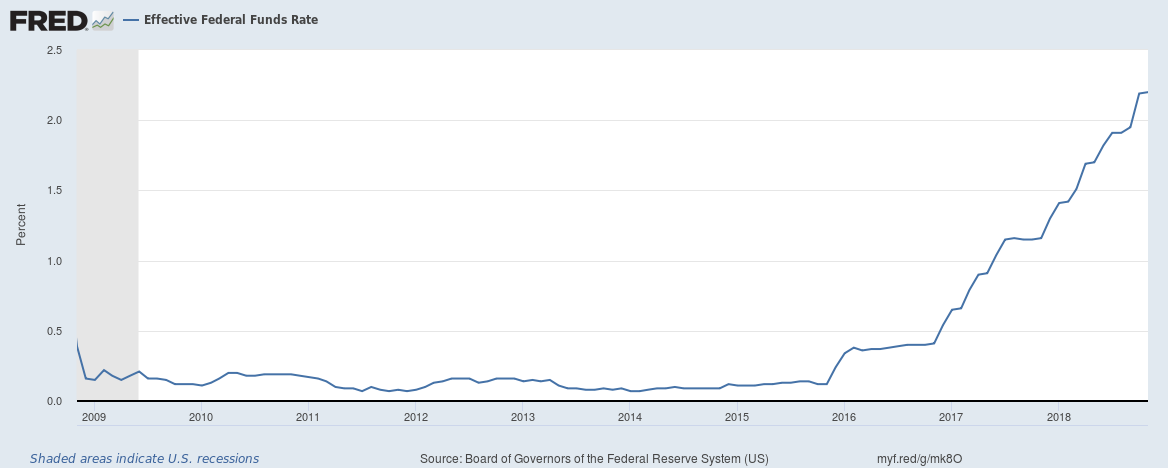

Inflation has steadily return in the US, something people have been looking for for years now. We are just around the Fed’s target of 2% CPI, and as such 2018 saw 4 increases in the Fed Funds rate from the FOMC this year. The target rate is now 2.25-2.50%.

In all there is little reason to believe that there are dangerous and perilous times ahead for the economy. Global trade may be slowly modestly (possibly an obvious consequence of a trade war) and US real estate may be less hot than it has been for a few years, but the average worker is well employed, finally seeing long-delayed wage increases and household and corporate balance sheets are healthy. American consumers are spending but not treating their homes as piggy banks this time around. Some sense of prudence and stability appears to have taken hold in our minds, for the time being. Could we see a recession soon? Sure. It’s always possible. Does it mean you should be worried about the health of a solid long-term financial plan? Absolutely not. Investing as if we’d never see another recession or bear market is life in a fantasy world, not the real world. We’re here to do real-world work and succeed in it.