2019 was an absolute blowout year for the US stock market, period. Gains of nearly 30% in any market in a single year is about as good as it gets (although more common than you probably think – this year wasn’t really an outlier by any historical standard). While nothing kept pace with large cap US stocks, many asset classes had good years as well, generating returns most investors would be thrilled with by themselves. In all it was a capstone year for one of the best decades in recent history.

Bonds did well as interest rates moderated, with the Barclay’s Aggregate up 8.72% for the year. Risk assets did well as corporate bonds and junk bonds outperformed their more stalwart US Government counterparts.

For all the complaining about diversification of late, international stocks had a fantastic year, up 18.44% as well. Emerging markets were also up strong double-digits (15.42%). Even one of the worst performers, the energy sector, was up over 8%.

The hardest part of 2019 was that diversification still hurt. Once again, as in several recent years, owning anything other than large cap US stocks led to lower returns. The question for investors is – what is your benchmark? Thoughtful investors with solid investment policy statements know several things:

1) Single calendar year returns mean very little.

2) Diversification works over time, not all the time.

3) We’ll never have the best returns, or returns as good as the best performing asset class in one year.

Comparing your portfolio returns to the S&P 500 is inappropriate, dumb, and guarantees you’ll be disappointed often.

Ironically in the last few months I’ve heard two loud and directly conflicting narratives from investors:

- US stocks are obviously expensive/overbought/”due” for a fall and we should get out; or

- US Stocks are obviously the only game in town and we should own more of/only own them and get rid of underperformers.

Here’s my narrative:

It sure has been a great year/run/decade for US stocks. I have no clue if they are “expensive” relative to history, current earnings, future earnings or other asset classes. I don’t believe that we are “due” anything from markets, be it corrections or ongoing bulls. There have always been, and will continue to be, those who believe that what just happened in markets will be what happens next (momentum) or that what just happened in markets means the opposite is coming soon (mean reversion). What I do know is that you are not going to get the timing right, period. You don’t know what comes next, I don’t know, so let’s quit pretending and go back to having a framework from which we make long-term investment decisions. We’ll take great markets when they come, but they won’t change what we do next. Period.

Economic Update

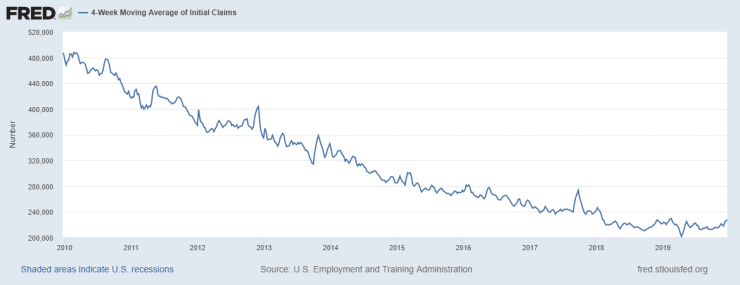

Weekly initial unemployment claims fell to 222,000 for the most recent full week of December. Claims remain very low by any recent historical standard. Prior data from October reported nearly 7.3 million job openings in the US, well above the reported number of employed workers (5.8 million) at the same time. Job openings were up 235,000 from the prior period as the labor market continues tightening. This is also reflected in the quits rate which continues to grow.

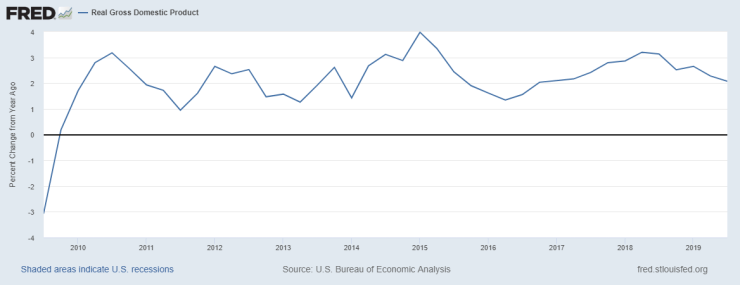

US Real Gross Domestic Product grew at a 2.1% annualized rate in the third quarter, generally keeping in the same long-term trend we have seen for several years now.

US Real Gross Domestic Product grew at a 2.1% annualized rate in the third quarter, generally keeping in the same long-term trend we have seen for several years now.

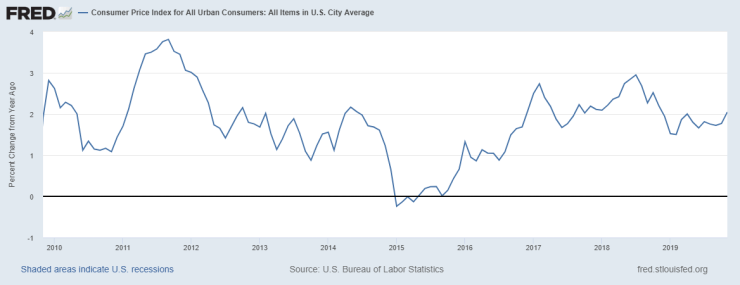

US Inflation remains muted as recent CPI readings came in at 2.0% in November over the previous 12 months. This is also reflected in the broad bond markets as long term rates fell again in 2019.

US consumers and households continue to see improvements in broad financial measures. The November BEA personal income and outlays report showed a monthly increase of 0.5% in disposable personal income and growth of 0.4% in personal spending. The US household savings rate remains healthy, nearly 8%, and household debt service (as a percentage of disposable income) is still very low, indicating that households are not over leveraged.

Tax, Legal & Legislative Updates

In previous updates I discussed the possibility of the passage of the SECURE Act through US congress, and in a last-minute push (as always), the SECURE Act was attached to a congressional spending bill in December. It was passed through the Senate and signed into law by the President.

There are several changes that will be in place going into 2020 and beyond. Perhaps the most significant is the elimination of the “stretch” IRA distribution, replaced with a mandatory 10-year window in which all inherited (by non-spouse beneficiaries) retirement accounts must be completely distributed. For many investors this could mean a larger tax burden for their beneficiaries. This could create incentives for current IRA holders to consider Roth IRA conversions if the tax burden on their heirs would be materially larger than that of the current account holder. Additionally, the 10-year window does not mean that assets must be evenly distributed over that period, providing some flexibility about the timing of those distributions and tax planning opportunities.

IRA account holders planning on using trusts (including trusts with “look-through” provisions previously designed to comply with Stretch distribution rules) may find that the trust needs to be amended to comply with new rules and prevent a single lump-sum distribution of inherited IRA assets in one calendar year.

Other changes now in place with the final legislation include:

- Extending the minimum age for required distributions from 70.5 to 72;

- Allowing IRA holders over the age of 70.5 to make annual contributions (previously disallowed), assuming the IRA holder or spouse has earned income;

- Making it easier for 401(k) plans to include annuity products in plan offerings with little need for fiduciary obligations around those annuities;

- Making it easier for small businesses to band together to join a 401(k) plan;

- Increasing the tax credit for small business 401(k) plans;

- Reducing the medical expense threshold for itemized deductions back to 7.5% for 2019 and following years;

- Allowance of the use of 529 plan funds to pay for student loans. In many states, this creates an incentive for student loan holders (or their families) to first fund a 529 plan and then withdrawal the funds to repay student debt;

Overall these changes mean new considerations for retirement savers and tax payers in general. As you go about planning for 2019, 2020 and beyond be sure that your investment, tax and legal professionals are taking these changes into account for your personal situation.