Global stock markets were again a bit tumultuous this quarter as July turned into August. The S&P 500 fell from a high of 3027 to 2839 in a matter of days, giving us all a nice reality check to how stocks typically behave! Despite this temporary free-fall feeling, US stocks finished up for the quarter with the S&P 500 gaining 1.70%. REITs and bonds also gained, but international stocks and emerging markets fell against a strong dollar. It’s important to realize that 2019 has been a great year for stocks, particularly US stocks. Bonds have performed well alongside equities. Even international stocks have posted near double-digit returns through 9/30/2019. So when it feels like the world is coming apart at the seams every time the market falls 5-10%, let’s take some perspective and recognize what an incredible bull market in US Stocks we have been party to over the last decade.

Economic Update

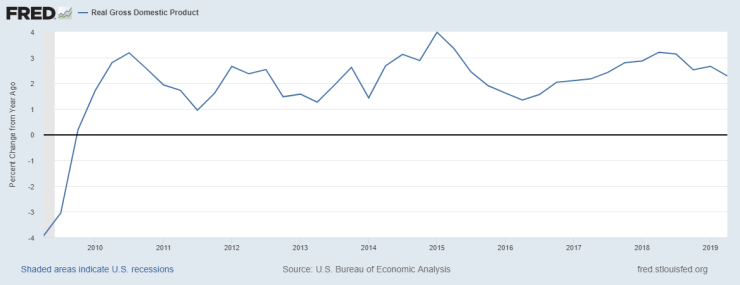

Economic growth has been largely unchanged, staying within a range of 2-3% for the last several years. The official measurement of real GDP growth for the second quarter of 2019 was 2.3%.

Despite a small drop in the rate of GDP growth, many economic indicators are trending positive. In labor markets, we are seeing ongoing tightening as available labor is surpassed by employer needs and wages are rising.

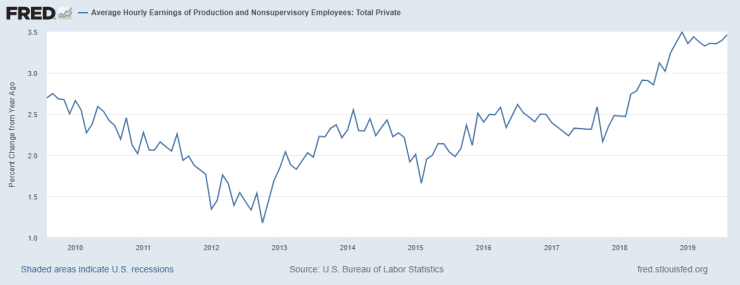

Average hourly earnings continue to move up, with growth of 3.5% year over year in August.

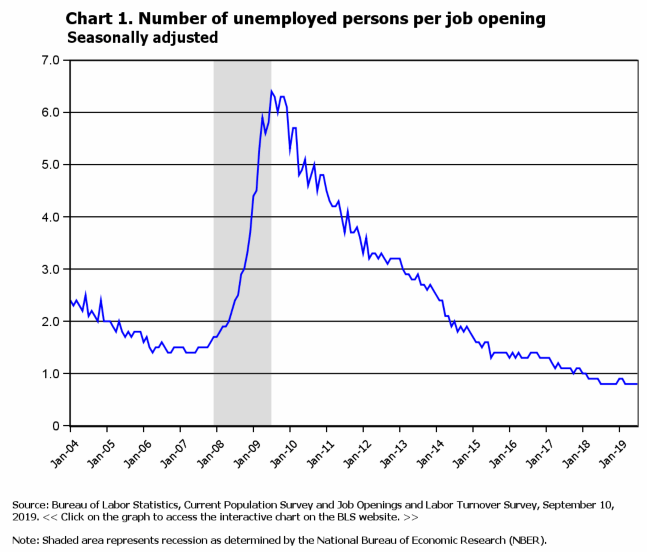

There is now fewer than one unemployed participant in the labor market for every available job opening, down from over 6 at the peak of the recession:

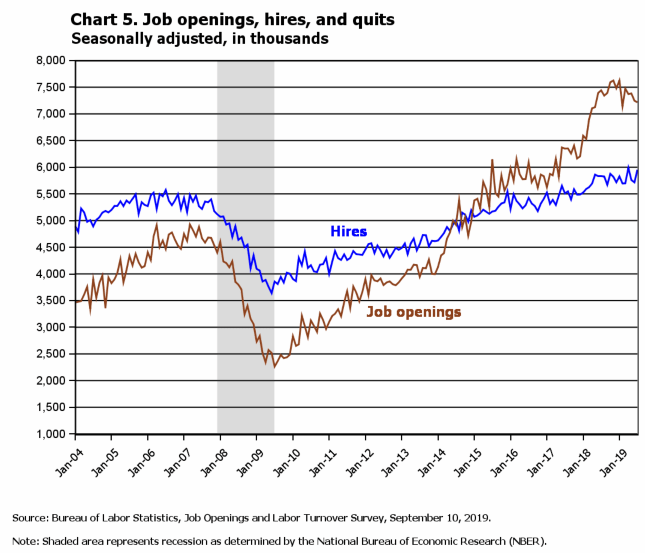

And employers cannot keep up with their need for staffing – employers are creating job openings faster than they can hire staff.

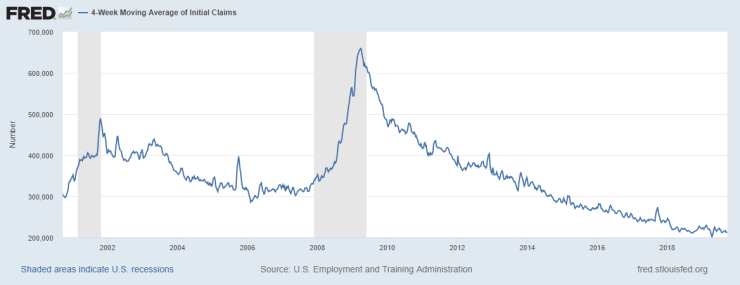

As a result, weekly new unemployment claims are hanging around decades-long lows with no material change in the 4-week moving average for some time. The trend has been very clear since the end of the recession in 2009 – ongoing tightening in the labor market with fewer and fewer workers without a job. Unemployment claims are well below previous pre-recession lows during the peak of the housing bubble and the tech boom.

Broader economic indicators are healthy, as US industrial production rose 0.6% in the month of August after a small decline in July. This puts the production index still above pre-recession peaks and near all-time highs.

Housing activity also remains solid. Current homeowners and borrows are in excellent shape. Foreclosure starts (at 36,200 for the month of August) were the lowest on record since December of 2000. Refinancing activity has been strong this year as rates dipped, putting more borrowers on solid footing. Active inventory of foreclosed homes is at its lowest level since 2005. Delinquent loans rates are still falling, now down to just 3.45% of all outstanding mortgage debts.

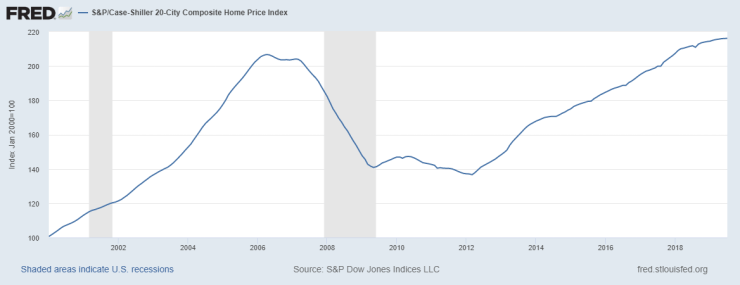

Home prices have steadily gained, with the Case Shiller 20 city national index up 3.2% in July over the previous year.

Home buying activity is also healthy, with new home sales up 6.4% year to date through August compared with the same period in 2018.

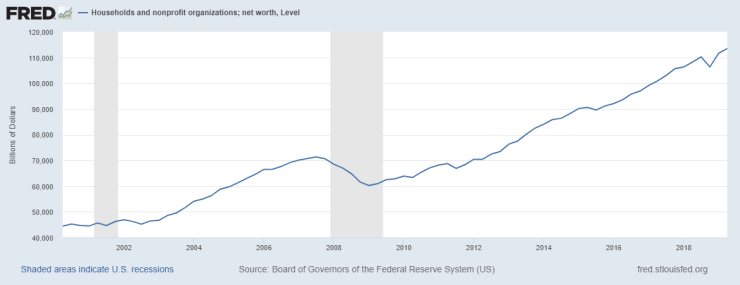

With all of this and strong stock markets, household net worth in the United States continues to trend upward, reaching new highs and well, well above pre-recession levels.

The big picture is this: while this economic expansion has often felt lackluster, the facts show that it has led to real economic improvement in large part due to the steady nature of low growth and the unusually (by historic standards) long duration. We haven’t seen bubble-like markets in major assets, nor frenzied borrowing and buying that has sometimes led to economic overreach and subsequent correction in the past. If the economies of the late 1990s and mid 2000s were the hares, we’re living in the tortoise’s world now. There will always be bumps, hiccups and scares along the way, and eventually the economy will get hit hard by something very few of us saw coming. But the trajectory over the last decade couldn’t be more clear: low, steady, long, and largely uninterrupted growth.

Tax, Legal & Legislative Updates

As of September 2019 the biggest news out of Washington is the potential passage of the SECURE Act, the largest overhaul of retirement savings law for some time. Supporters of the legislation, which passed with an enormous majority in the House (417-3), are hoping to attach the bill to a mandatory spending bill that would keep the Federal government open. Last week President Trump signed a continuing resolution to fund the government through November 21st, at which time another continuing resolution or a permanent spending bill will need to be passed to avoid shutdown. Current news out of DC is that Senate majority leader Mitch McConnell is unlikely to bring the bill to a floor vote, so attachment to a spending bill is the best option the bill has of passing.

As outlined last quarter, the SECURE act would change a number of key retirement savings rules, including:

- Extending the minimum age for required distributions from 70.5 to 72;

- Terminating lifetime inherited IRA distributions in favor of the 5-year rule;

- Making it easier for small businesses to band together to join a 401(k) plan;

- Increasing the tax credit for small business 401(k) plans.

The most material of these changes for most investors is the possible elimination of lifetime distributions of inherited retirement accounts. Forcing full distributions of retirement assets over a 5-year window will increase income tax planning for most beneficiaries and would cause many investors to revisit their current estate plans. This rule change could make charitable giving from retirement accounts or Roth conversions more attractive strategies. For now, we will wait and see if the legislation can come through the Senate.