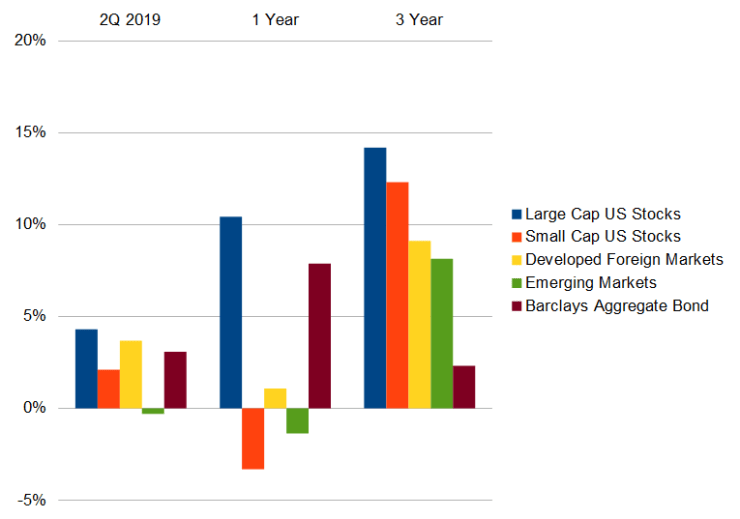

Markets gave investors a brief scare in May with a mid-period decline of around 7% attributed to ongoing trade war concerns, but recovered quickly. Once again US stocks had a very solid quarter with overall gains of 4.30% for the S&P 500 for the three months ending 6/28/19. Small cap stocks (+2.10%) and developed international markets (+3.68%) also posted solid returns for the quarter. Bonds were steady again with positive returns of 3.08% for the Barclays Aggregate index.

We find ourselves again in a now familiar story: generally calm markets (a 7% decline is newsworthy?!), steadily upward moving stock prices (led primarily by US large cap stocks) and an overall absence of volatility, leaving investors comfortably relaxed. Which is great! Investors should be relaxed. But we should be relaxed all of the time, not just when markets are friendly as they have been recently. If we can be relaxed now, we need to remember the feelings of panic and fear that can easily creep in when stock prices aren’t quite so calm. We will, someday, have a real bear market again. The kind of market that convinces investors they are doing everything wrong, that the world is coming apart at the seams, that economies will come to a permanent state of free fall. When that happens, it’s key to remember that nothing has inherently changed about the world for 99% of the population. People keep going to work, looking for work, taking steps to improve their lives and their children’s lives. Yes, recessions come and yes, they are unpleasant and feel largely unproductive. But recessions also end. Accepting the permanently cyclical nature of economies and markets is a must for the long-term investor. Recognizing where we currently are in that cycle goes a long way to making the other side palatable.

Economic Update

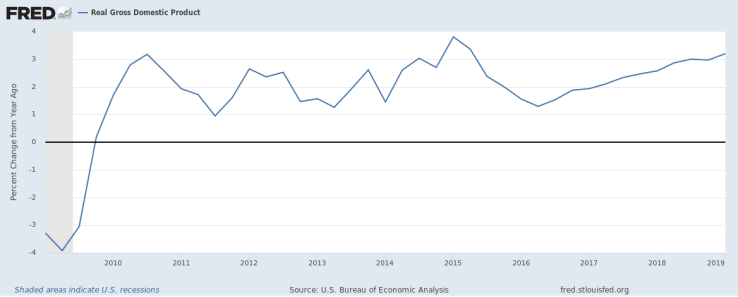

Economic growth was strong in the first quarter, with real GDP coming in at 3.2% annual growth over the previous year. The trend has been positive for the last several quarters and 1Q represented an increase over the previous quarter. Estimates for 2Q GDP growth are around 1.5%.

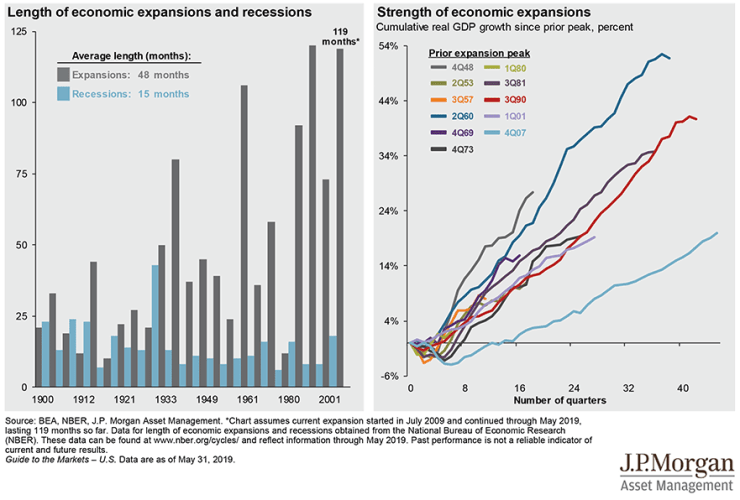

Many people will continue to cry that the economic expansion is “long in the tooth” (it is) and thus a recession must be imminent (not necessarily). It is worth considering that despite the age of the expansion, the overall level of economic activity from the previous economic peak remains subdued given the low level of overall economic growth during the expansion.

Recently release household finance and consumer spending figures look strong. Personal consumption expenditures grew 0.4% in May over April and annual growth has been strong.

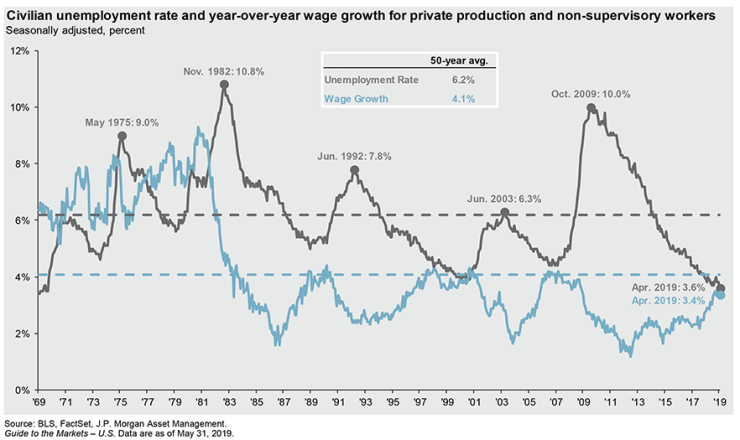

The labor market remains solid as unemployment sits at 3.6%, well below a long-term average. Wage growth continues to slowly move up, with annual gains of 3.4% (nominal) in April over the previous year.

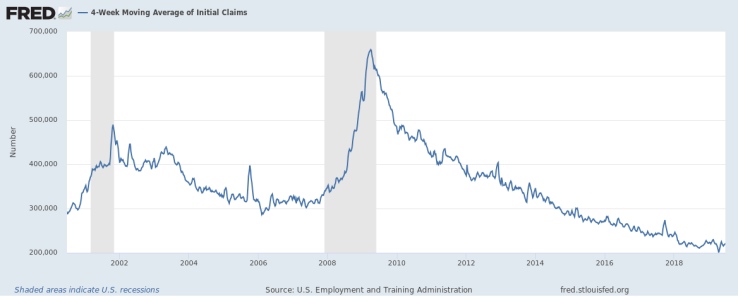

Initial jobless claims have moved up a nearly indiscernible amount from the recent bottom, but the 4-week moving average of initial claims sits near historic lows.

The housing market also remains robust and generally stable. Rapid increases in national home prices have cooled and year-over-year increases through April were a more typical 3.5%.

Mortgage activity increase as the markets remain active for transactions and refinance activity increased with long term market rates falling close to 4% again this quarter.

Mortgage delinquency rates continue to fall. Freddie Mac reported that in May serious delinquency rates (3 months past due) fell to 0.63%, down from 0.65%. During the crisis peak serious delinquencies made up 4.20% of Freddie Mac reported mortgages.

Tax, Legal & Legislative Updates

Actual policy information and activity from Washington has been quiet, with little new policy of impact to investors and taxpayers since the major changes to the tax code for 2018.

Bloomberg reported last month that the White House is considering legislation that would index the cost basis of an investment to inflation, ultimately reducing capital gains exposure for investors to “real” growth. However, these proposals have been made in the past and rarely see the light of day, so we should likely not put much stock in this idea for now.

One consequence of the 2018 tax reform was limits on taxpayer’s ability to itemize and deduct state and local income taxes, capping a Federal deduction at $10,000. This led to states trying to get creative and find workarounds for the residents to retain the tax benefit. Last month the IRS officially issued guidance to disallow these schemes, including having taxpayers make “donations” to a state “charity” and receive equal tax credits, effectively turning tax payments into a false charitable contribution. This creative money shuffle and others like it are now DOA.

Possible changes are on the horizon for retirement accounts, taxes and regulations for American investors. In May the house passed the SECURE Act of 2019, which would increase the beginning age for Required Minimum Distributions from 70.5 to 72, allow IRA contributions beyond age 70.5 and increase allowances for non-retirement distributions including birth and adoption expenses.

Notably, the House legislation could also eliminate “Stretch” IRAs, or the ability of a recipient of an inherited IRA account to take distributions over his/her lifetime. Instead, retirement account assets would be forced to be distributed over a 10 year horizon, often increasing tax liability as a result. I’m keeping my eye on this one as it has potentially large implications for long-term tax planning for retirees.

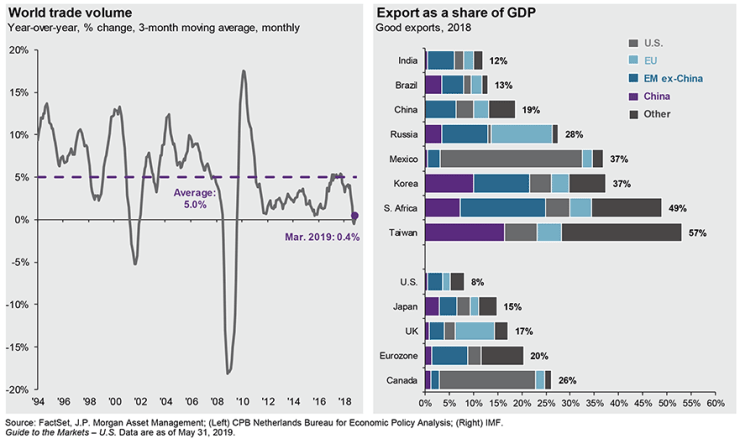

Finally, ongoing concerns over global trade shook markets in May as President Trump made threats toward Mexico regarding further increases in import tariffs on Mexican goods. This threat has stalled for the time being, but it is clear that these continuous trade barriers have had a material impact on global trade activity. Growth in global trade ground to nearly a standstill early this year, a dramatic fall from the historical 5% average we had seen prior to tariffs and retaliatory tariffs among global trading partners.