It is getting harder and harder to talk about “markets” as if they are one collective organism and not a diaspora of individual companies, succeeding and failing, gaining and losing public favor, having great runs and terrible stretches. I could say that “the market” is up over the last twelve months but that would be a terrible description of what has really happened.

What has really happened is that a handful of very popular, very large, very tech-oriented US stocks have had a spectacular period. And a whole lot (okay, the majority by gross number) have had a year ranging from mediocre to abysmal. The dispersion of returns between the best and worst stocks and sectors, just in the US, has been enormous. As of this writing, Apple (AAPL) is up over 108% in the last twelve months and small cap value stocks (Russell 2000 Value) are down -14.88% in the same period.

This is why it is really dangerous to talk about “the market” and what “the market” has done recently. “The market” is just an average, and that average depends on what is included in your average, and it’s pretty easy to have a head-in-the-oven-feet-in-the-freezer situation there, not unlike what we have seen recently. It is especially important to take these concepts into consideration when trying to compare your portfolio performance to “the market.” If your portfolio is balance (some stocks and bonds), global (not just US stocks), inclusive of small caps and/or tilted toward value, the odds of you “keeping up” with the S&P 500 in a year when tech bro stocks are blowing up are just about 0.000000%.

Economic Update

The global economy is slowly trying to claw its way out of the massive decline experienced early this year as a result of pandemic shutdowns. Many indicators of employment, industry and income are moving in the right direction, but with a long way to go to see pre-pandemic levels.

In August, US employment grew by 1.4 million jobs but the unemployment rate remained very high at 8.4%. Many people have returned to work as businesses slowly reopened but we have a long way to go. The economy still has over 10 million fewer jobs than it did a year ago in August 2019. August 2020 employment figures included temporary hiring for census workers, so it is possible that September numbers could be lackluster in comparison. Peak unemployment during the pandemic was significantly higher than any level during the financial crisis and continuing and new unemployment claims remain elevated.

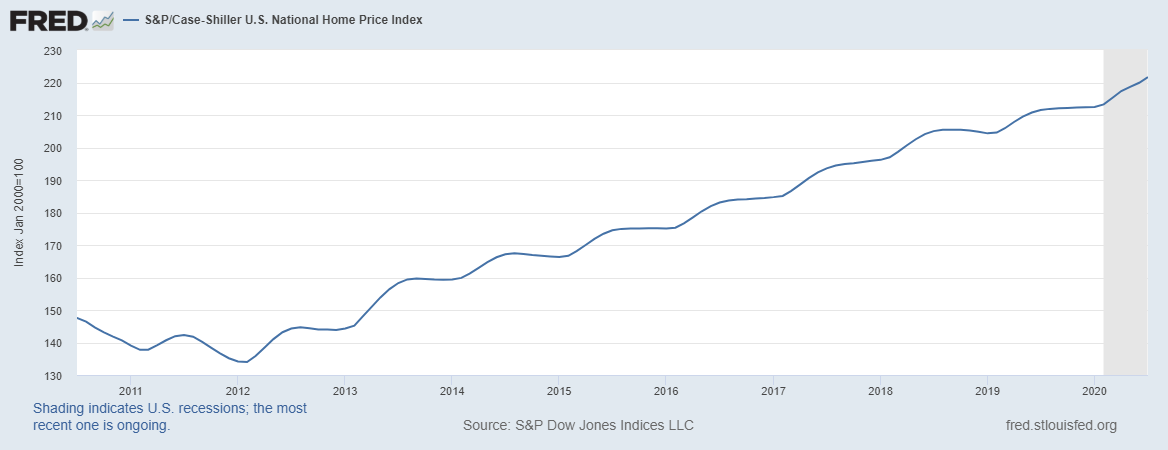

Housing is a bit of a bright spot, as least as prices are concerned. Record low mortgage rates and limited housing inventory have pushed prices higher nationwide. The Case Shiller national housing price index increased 4.8% year over year in July. Individuals and families not affected by unemployment related to the pandemic are taking advantage of low rates and boosting home market activity. Existing home sales in August were at their highest level since 2006.

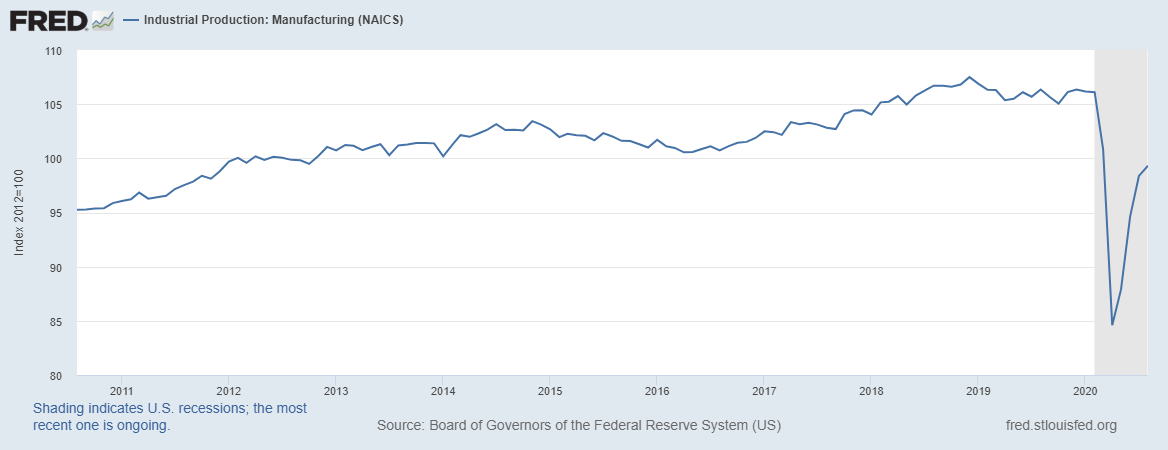

Commercial and industrial activity is showing signs of a return to healthy activity as well. The Richmond Fed reported that September manufacturing activity increased and producer confidence is high as well. Industrial production nationwide is trending higher though still well below pre-pandemic levels.

Vehicle sales tell a similar story with an enormous drop in sales in early 2020 and a rebound since, but levels are still well below sales from a year ago.

Tax & Policy Updates

After the passage of the CARES Act in March, there has not been a great deal of policy news out of Washington. The CARES Act, among other things, created forgivable small business loans, provided advance tax credit payments to most American households of $2,400 per married couple, boosted tax deductions for charitable giving for those who don’t itemize and suspended required minimum distributions from retirement plans for the year 2020.

As of this writing, much has been discussed about a second round of economic stimulus but legislative gridlock has resulted in lots of talk but no action. At the very tail end of September, it appears that House Speaker Nancy Pelosi and house Democrats are working on a new $2.2 trillion package and in discussion with Treasury Secretary Steven Mnuchin. The proposal would include reintroducing the $600 increased unemployment benefit and an additional round of $1,200 stimulus checks to taxpayers. While it is possible that the House could vote on (and pass) this legislation before election day, there is great skepticism that the Senate and White House will quickly approve the passage.

Separately, there has been considerable hand-wringing around Democratic Presidential nominee Joe Biden’s tax proposal, which would increase income taxes on taxpayers in the top bracket (over $400,000 in taxable income) and make changes to estate taxes and capital gain tax rates for top bracket payers. I really only have two thoughts about this:

- Joe Biden is not yet president of the United States, so let’s relax a little.

- No president has ever unilaterally had a proposal about taxes or any other legislation become law as proposed.

The election is a heated matter for parties on all sides, but it’s important to remember that US Presidents are not dictators. The office does not come with a magic wand that instantly creates the world they may imagine, or a special dial that creates or destroys economic growth. The world is an immensely complex place and no single person can exert control over it, regardless of his or her position.

Just about every election cycle I re-up a piece that I wrote in 2012 about why the election noise is nonsense for a long-term, diversified investor. It’s still every bit as true today. While we may have some year-end planning to consider after the election, your long term philosophy should be untouched by the handing over of White House keys.