What a year. What is there to say, other than that it’s behind us now. For many of us it was long, trying and taxing just to be humans over the last twelve months, let alone investors. There was (is) a global pandemic, a presidential election, a major bear market, a bull market, and the most rapid explosion in unemployment in US history, to name a few. One stimulus bill, and now another.

Amidst all of this madness, stock markets put up a surprisingly good year. For a change, small cap US stocks have beaten out their large cap counterparts over the last twelve months, up 19.96% vs. 16.26%. International stocks were also positive, and bond returns were remarkably strong as long term interest rates fell during the pandemic.

You could look simply at these one-year numbers and assume that everything was smooth sailing, but markets have never been smooth sailing and this year was certainly no exception. The markets peaked early in the year on February 20th, only to experience a sudden and precarious drop through March. This period included some terrifying days where investors saw US stocks decline over 7% multiple times. On March 20th, the DJIA fell nearly 13% in a single day, following closely behind a drop of nearly 10% the week before.

And then, while things seemed incalculably terrifying, markets starting climbing again. By late summer the S&P 500 was reaching new all-time highs.

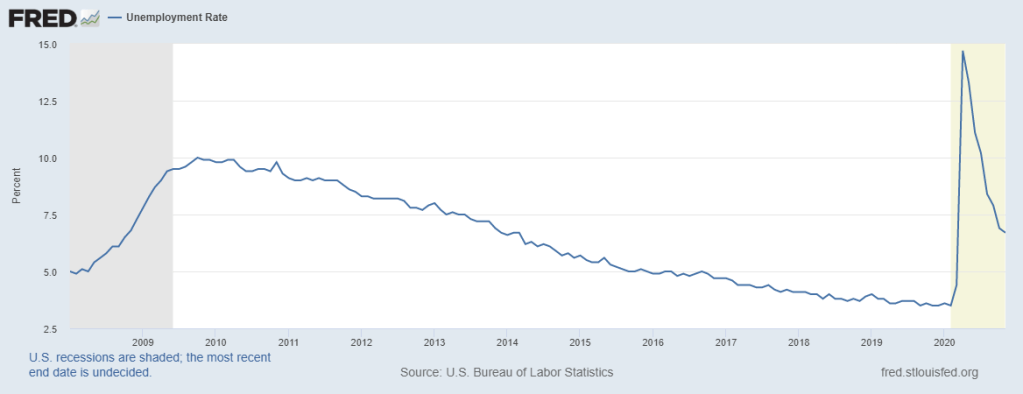

I almost wish that I had a public diary of my day to day thoughts during the spring. I actually wish we all did. It is so easy now to look back and shrug off this massive market meltdown as a brief, panic-induced flash. But I can guarantee you that was not your initial thought in March of this year. It was scary. Period, full stop. It felt different this time, and it was. 30% market declines are not supposed to happen in a month. Unemployment is not supposed to jump from 3.5% to 14.7% over 8 weeks. This wasn’t how it was supposed to work!

If we have learned anything from all of this, it should be that markets are unpredictable. I’m constantly saying this in calm markets and in bad markets. You and I will not predict the timing or circumstances of the next bear market, just like we won’t pick the next Tesla or short the next Casper. We don’t know the outcome of the next election cycle or how that outcome might impact markets.

My professional life is a broken record. The goal here is to admit our limitations and avoid our likely failures as best we can. Right now there are people trying to predict the outcomes of the GA runoff senatorial elections, the direction of interest rates next year, the best sector for 2021, what a Biden presidency means for turnstile manufacturers in Iowa and millions of other things. I have zero confidence that I or anyone I know can accurately play that game, so I am going to sit it out and advise you to do the same. The best long-term prediction I can make is that we’re going to keep having bear markets and they will all end eventually with new all-time highs. That’s the bet we make as long-term diversified investors because it is the one that historically and statistically has paid off the most reliably over time.

Enough of that. Here’s what markets looked like in the rear view.

Economic Update

It is almost impossible to write normally about the activity levels of the global economy in 2020. If you had “global health crisis” down as the reason that the longest economic expansion in history would come to a crashing halt, I’d like to talk to you about your thoughts on the next Superbowl champions as well. A broad, self-imposed shutdown of most of the economy this spring led to a collapse in year-over-year economic growth. Growth contracted 5% in the first quarter and then an unheard of 31% in the second quarter, only to rebound 33% in the third quarter. This numbers are so incomprehensible as to render them meaningless. Most full-year estimates reflect a 4-5% reduction in global economic output for 2020.

Since the spring, we have been slowly clawing our way back to some sense of normalcy, with a long way to go still. Initial unemployment claims are falling slowly but are still above any level seen in the 2008-2009 recession. Unemployment is falling as many of the jobs lost in the spring came back much more quickly than a typical recession.

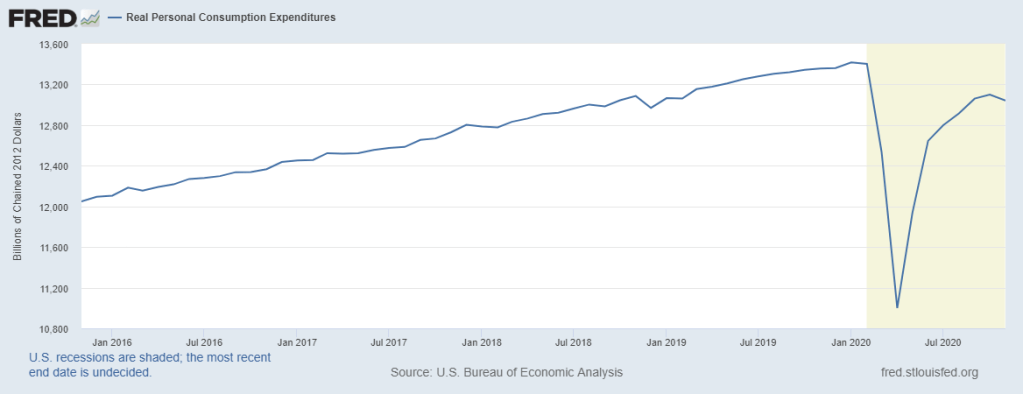

Personal spending has rebounded from the bottom but with a resurgence in COVID-19 cases late this fall, has dropped back off again. Real Personal Consumption Expenditures are well below early 2020 levels as consumers have limited opportunities and many Americans have limited means for personal spending.

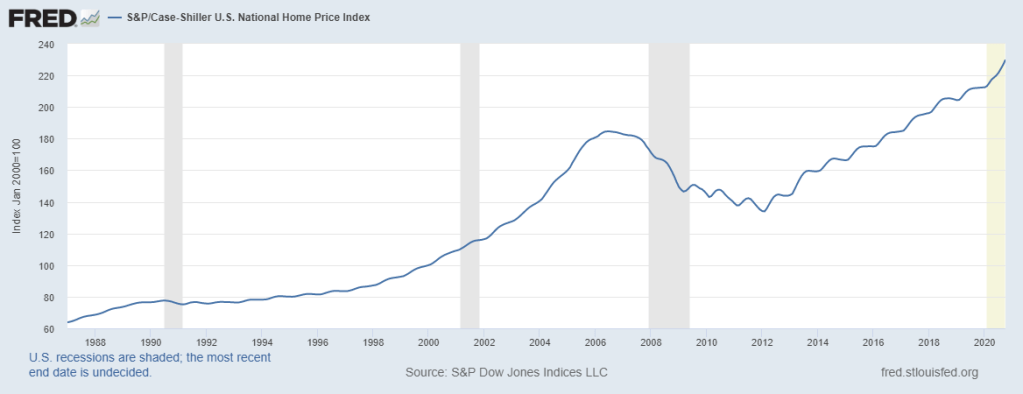

Residential real estate prices continue to boom, buoyed by falling interest rates and limited housing stock. Pandemic shutdowns caused a fall in new home construction and sales, and we all know the feeling (and some the personal experience) of looking for a new home to be locked down in. In October the Case-Shiller National Home Price Index had gained 8.4% over the previous twelve months, again reaching all time highs. Looking only at this data, you could never know the economic turmoil we experienced in 2020.

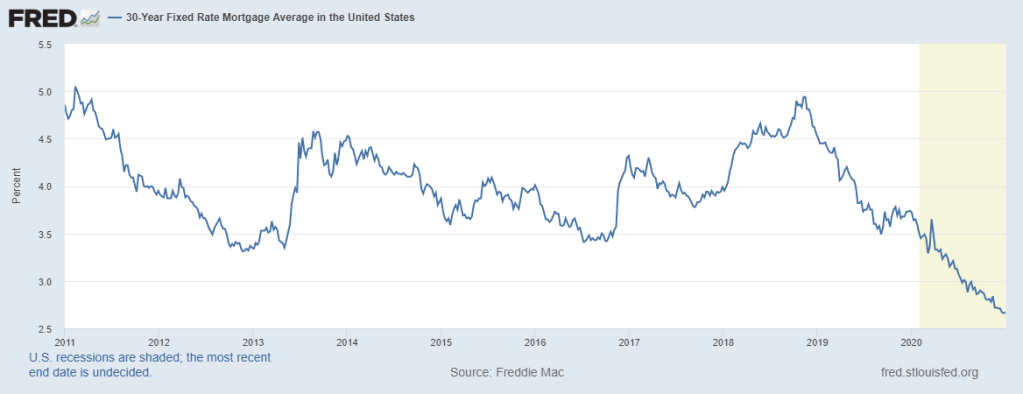

Mortgage rates are at historic lows, spurring incredible refinance activity and boosting home prices as we saw above. National average rates for a 30-year loan touched 2.66% late in 2020 (and here I thought my 15-year, 2.875% mortgage was a steal in September!).

Tax & Policy Updates

First, just one quick comment about the election: the world did not come to an end as many conservative-leaning investors thought it might, and the world has not been miraculously changed as some liberal-leaning investors may have expected. We are still here, we are still us, and the same will be true after the next election cycle and the one after that.

While we now know that Joseph Biden will be the next President of the United States, we still await the results of the Georgia senatorial runoff elections to see which party will have control over the upper house of Congress: if we will see Democratic control over two branches of government or a divided balance of power. It is reasonable to assume these two outcomes could result in materially different legislative priorities, but that does not mean one will be horrific for markets and one will be wonderful. The world doesn’t work that way, just like the economy didn’t care who was in office when the real estate bubble popped in 2007-2008, who was in office as we dug our way out of a massive recession for ten years, and who was in office when a global pandemic took the world by force. Good and bad things happen regardless of whether the President wears a blue tie or a red tie.

More importantly, at the midnight hour Congress passed, and President Trump signed a second major stimulus bill for the year. A quick summary of the new bill passed on December 21st follows.

- A second round of direct stimulus checks of $600 per person for individuals earning less than $75,000 per year (married couples less than $150,000).

- Extended additional unemployment benefits of $300 per week for 11 weeks.

- Businesses that experienced major losses in revenue will be eligible for a tax credit for retaining their employees.

- An extension on the deductibility of charitable giving in 2021 up to 100% of adjusted gross income.

- Expanded Lifetime Learning Credits for 2021, including a materially higher phaseout range ($160-$180,000 for married filers).

- An expansion of the Paycheck Protection Program from earlier this year, allowing businesses who had not yet received a PPP loan to apply for a first loan, and businesses still struggling because of the pandemic to apply for a second PPP loan under tighter restrictions than the first round.

- Clarification on the deductibility of expenses covered by PPP loans, eliminating the possibility for a tax “penalty” against otherwise normal business expenses.

- PPP loans under $150,000 will have simplified forgiveness applications and expedited approvals for forgiveness applications.

- Notably, the waiver of Required Minimum Distributions for 2020 introduced in the CARES act earlier this year was not reintroduced and will not apply for 2021.

As ever, we will take these legislative changes into account when planning for your financial future, and we will give less credit to political grandstanding, blame-pointing and credit-taking for everything else that happens in the global economy and markets.